Thinking about the future of your Ontario business? Exiting your business is a major milestone, and planning it carefully can make all the difference. Many business owners worry the process will be complicated, costly, or time-consuming. But with a clear exit strategy, you can maximize your business’s value, avoid common issues, and ensure a smooth transition for everyone involved.

In this guide, we’ll cover the key steps to building a straightforward, effective exit plan. From setting your goals to meeting Ontario’s legal and financial requirements, you’ll learn how to approach your business exit. Whether you plan to sell, transfer ownership to your family, or explore other options, a well-crafted exit strategy is key. Let’s dive in and get you started.

Did you know that based on the CFIB report, only 1 in 10 business owners (9%) have a formal business succession plan in place to ensure a smooth transition?

Insight Law Professional Corporation is a business law firm. If you’re ready to start planning your exit, seek professional guidance on creating a strategy that aligns with your goals. Contact a small business lawyer today if you require assistance with your business sale from start to finish.

What Is a Business Exit Strategy?

A business exit strategy is a plan that allows a business owner to leave their business with minimal risk and maximum benefit. This strategy outlines the steps needed to transition ownership, whether selling to a buyer, transferring to a family member, or another method.

An exit strategy assists the owner in maximizing the business’s value, minimizing potential risks, and meeting legal and tax obligations. By planning an exit, owners can prepare for unexpected events and make decisions that align with their goals.

Exit strategies vary depending on the owner’s objectives. Options include selling to an external buyer, passing the business to family, or considering a management buyout. Each choice has unique benefits, which we will explore further in upcoming sections.

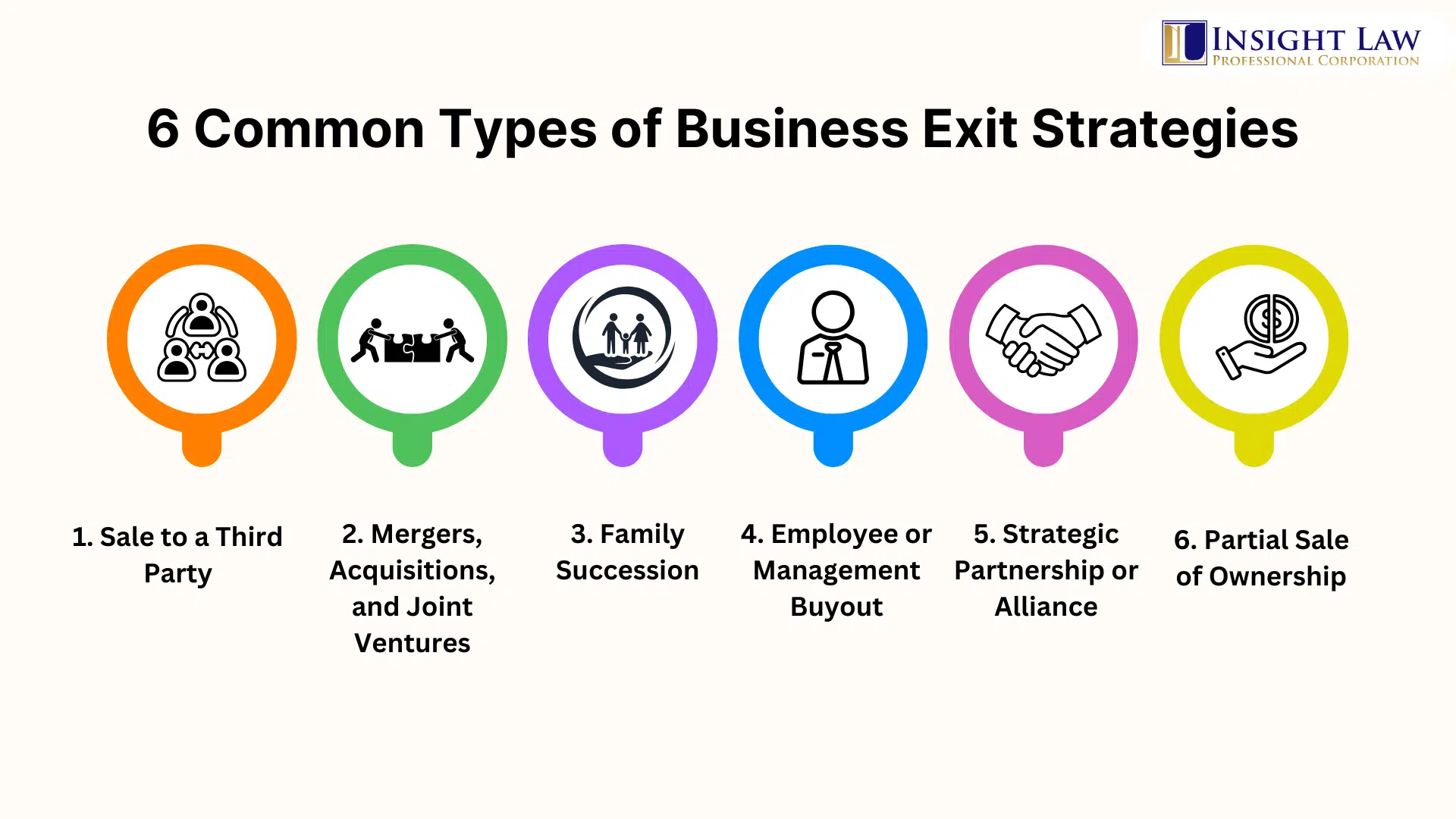

Types of Business Exit Strategies

Here are the most common exit strategies, with their advantages, challenges, and practical examples:

1. Sale to a Third Party

In a sale to a third party, you transfer ownership to an outside buyer, such as a competitor or investor. This approach provides a clear exit with a one-time payment, offering the owner a quick and often profitable transition. However, after the sale, the new owner may change the business’s direction, which can affect employees and customers adapting to the changes.

- Pros: Offers a clear exit, provides a lump-sum payment, and allows a quick transition.

- Cons: Business direction may change under new ownership, which can impact staff and customer relations.

Example: A small tech company in Ontario is sold to a larger competitor. The original owner gains the freedom to start new ventures while the buyer integrates the brand, expanding its reach and market influence.

2. Mergers, Acquisitions, and Joint Ventures

Merging with or being acquired by another company enables the business to combine resources, expand its market, and increase its value. This strategy is popular in Ontario’s manufacturing and tech sectors, where companies benefit from shared resources and reduced costs. However, merging often brings challenges, such as cultural differences and complex legal requirements.

- Pros: Expands market reach, increases business value, leverages shared resources.

- Cons: Cultural differences may complicate operations; legal complexities require careful planning.

Example: An Ontario-based manufacturing firm merges with a national supplier, benefiting from resource sharing and a stronger position within the industry.

3. Family Succession

Family succession involves passing the business to a family member, ensuring continuity and preserving the owner’s legacy. This strategy is ideal for those who want to keep the business within the family. You may also need to train them to manage the business successfully. This could take time, depending on the complexity of the business.

- Pros: Maintains family legacy, ensures business continuity, and offers a familiar transition.

- Cons: Potential for family conflict; Ontario tax implications may affect the transfer.

Example: A family-owned restaurant in Ontario prepared for succession by gradually involving the owner’s son in operations, ensuring a smooth handover that preserved the restaurant’s values and loyal customer base.

4. Employee or Management Buyout

An employee or management buyout allows trusted employees or managers to purchase the business, maintaining stability and company culture. This approach keeps familiar leaders at the helm, which can reassure staff and customers. However, securing financing can be difficult, and the new owners may face additional responsibilities.

- Pros: Retains company culture, provides continuity, and smooths transition.

- Cons: Financing can be challenging; new owners may feel pressure from expanded roles.

Example: An Ontario retail store transitioned ownership to its management team, which secured a local business loan. This approach allowed the store to continue operating smoothly with trusted leadership.

5. Strategic Partnership or Alliance

A strategic partnership or alliance allows business owners to bring in resources from another company without fully exiting. This option is suitable for those who want to grow their business with external support while keeping some control. However, shared decision-making can lead to disagreements if partners have conflicting goals.

- Pros: Accesses external resources, supports growth, retains partial control.

- Cons: Shared control can create conflicts if partners have different objectives.

Example: A software firm in Ontario partnered with a national tech company, gaining access to a larger distribution network while the original owner retained partial involvement.

6. Partial Sale of Ownership

In a partial sale, the owner sells a portion of the company, allowing for outside investment while keeping some control. This approach brings financial benefits and enables the owner to stay involved. However, balancing control with new investors requires careful management.

- Pros: Provides capital for growth, retains owner involvement, allows the owner to maintain some control.

- Cons: Shared decision-making with investors requires clear communication and balanced expectations.

Example: An Ontario boutique sold 40% of its ownership to a private investor. This partnership provided funds for growth while the original owner continued managing operations and overseeing the expansion.

According to the CFIB report, the most common approach is to sell the business to someone unrelated to the family (49%), the second common method is to sell to a family member(s) at 24%, and the third most common method is to sell to employee(s) at 23%.

Method of exiting (% response)

| Method of exiting (% response) | Percentage |

| Sell to buyer(s) unrelated to my family | 49% |

| Sell to family member(s) | 24% |

| Sell to employee(s) | 23% |

| Transfer to family member(s) (e.g. inheritance) | 21% |

| Wind down (close) the business | 17% |

| Don’t know/Unsure | 9% |

| Sell to international buyer(s) | 9% |

| Other | 3% |

Note: The total does not add up to 100% because the respondents could select more than one response.

Why Planning Your Exit Early Is Essential

Here are some reasons why starting early is essential:

1. Early Planning Increases Control and Value

- Early planning gives you time to set clear goals, assess business value, and identify areas for improvement. By understanding your goals, you can focus on areas that will add value to the business.

- For Ontario businesses, planning early also aligns operations with local market and regulatory requirements, helping to avoid compliance issues later.

- A well-developed roadmap for growth strengthens your business’s appeal to buyers, increasing the chances of a profitable sale when the time comes.

2. Financial and Legal Preparedness

- Tax Compliance: Early planning helps you address Ontario’s tax requirements, including capital gains tax, which can significantly impact your sale proceeds. With time, you can explore exemptions, deductions, or other tax-saving options to reduce your tax burden.

- Required Documentation: Organizing contracts, permits, and financial statements in advance ensures that your business meets Ontario’s standards and regulatory requirements. Having these documents ready reassures buyers, speeds up the due diligence process, and reduces the chances of delays.

3. Minimizes Risks and Maximizes Opportunities

- Risk Reduction: Early preparation helps you address and resolve debts, liabilities, or legal issues that could impact the sale. By managing these risks ahead of time, you avoid last-minute complications that might weaken buyer interest or lower your business’s value.

- Market Positioning: Extra time allows you to monitor market trends and adjust business strategies to increase attractiveness. Refining operations, adjusting pricing, or diversifying offerings positions your business favourably in Ontario’s market, boosting its appeal and potential sale price. Identifying the best market conditions also helps you choose an optimal time to sell.

Planning your exit early can help secure the best outcome and reduce stress by allowing you to handle each step thoughtfully instead of facing last-minute pressures.

Reasons for exiting

According to the CFIB report, the main reason for owners exiting their business, by far, is retirement (75%). Burnout/stress is the second main reason at 22%. Step back from owner’s responsibilities is in third place at 21%. Other reasons include Selling our business to maximize our investment (15%) and due to not having a suitable successor (12%).

Reasons for exiting (% response):

| Reason | Percentage |

| Retirement | 75% |

| Burnout/Stress | 22% |

| Step back from owner’s responsibilities | 21% |

| Selling our business to maximize our investment | 15% |

| No suitable successor | 12% |

| COVID-19 impacts on our business | 11% |

| Business is not profitable enough | 7% |

| Move on to another business venture | 7% |

| No potential buyer | 7% |

| Other | 6% |

| Change career (start employment elsewhere, etc.) | 7% |

| Don’t know/Unsure | 3% |

Note: The total does not add up to 100% because the respondents could select more than one response.

Common Mistakes in Business Exits and How to Avoid Them

Here are key mistakes to avoid:

- Lack of Planning

Rushing into a sale without a clear exit plan can significantly reduce your business’s value and limit your options. Begin planning well in advance to avoid last-minute decisions. Set specific goals, establish a realistic timeline, and review your plan regularly to stay prepared and adaptable. A well-thought-out plan allows you to make strategic adjustments based on market conditions or changes in your business.

- Underestimating Your Business’s Value

Many business owners undervalue their business, often overlooking intangible assets like brand reputation, customer loyalty, or intellectual property, which can hold substantial worth. To avoid leaving money on the table, get a professional valuation from an experienced appraiser. Recognizing the full worth of assets like customer relationships or market position helps you achieve a fair sale price and avoid underselling.

- Incomplete Legal Documentation

Missing or disorganized legal documents can delay the sale process and deter potential buyers, as they may perceive it as a red flag. Work with a legal advisor to gather all necessary documents, including contracts, licenses, and tax filings, well in advance of listing the business for sale. Organized documentation shows that your business is well-managed and reassures buyers, making the transaction process smoother and faster.

- Not Preparing for Due Diligence

Many business owners overlook the due diligence process, which is required for building buyer confidence. Compile all required financial and operational records, such as up-to-date financial statements, tax filings, and employee agreements, ahead of time to make the review process easier for buyers. Clear and organized documentation gives buyers a complete picture of your business’s health and helps to avoid delays caused by missing or incomplete information.

- Neglecting Employee Communication

Sudden ownership changes can unsettle employees if they’re not informed early. Poor communication can create uncertainty, affect morale, and even lead to employee turnover, which could impact the business’s stability and appeal. Keep employees updated about your exit plans and, when appropriate, involve them in transition discussions. Open communication shows respect for your team, helps retain key employees, and supports continuity as new ownership takes over.

- Ignoring Market Timing

The timing of your exit can have a major impact on the sale price, as market conditions play a significant role in buyer demand and valuation. Monitor economic trends, industry performance, and competitor activity to identify the optimal time to sell. A well-timed exit strategy helps you maximize your business’s value by taking advantage of favorable conditions and high demand in your market.

- Inadequate Preparation for Handover

A successful exit requires preparation for a smooth handover, which ensures that the business remains stable under new ownership. Consider training a successor, if possible, or creating detailed documentation of essential business processes, key contacts, and customer service practices. This preparation eases the transition for the buyer, preserves the business’s value, and helps maintain customer and employee satisfaction during the ownership change.

Exit Strategy Timeline: How Long Does It Take?

Creating and executing an exit strategy takes time and careful planning. For Ontario business owners, understanding the typical timeline helps set realistic expectations and ensures that important steps aren’t rushed. Here’s a breakdown of the main phases involved in an exit strategy:

- Initial Planning (Typically 1–3 Months)

During the initial planning phase, set clear exit goals, conduct a preliminary business valuation, and create an outline of the exit plan. This is the time for Ontario business owners to decide what they want from the sale—whether it’s maximizing value, ensuring continuity, or selecting a specific successor. Establishing these goals and performing an initial assessment sets the foundation for a structured exit process. A solid exit plan created during this phase will guide decisions in later stages and help avoid surprises.

- Preparation (Usually 3–6 Months)

The preparation phase focuses on enhancing the business’s attractiveness to buyers and ensuring all legal and financial documents are in order. Ontario business owners should work with advisors to review contracts, update financial records, and identify and address any operational inefficiencies. This is also the time to organize employee roles, assess any customer or supplier contracts, and ensure compliance with Ontario regulations. Legal and financial preparations can be time-consuming, so starting early helps ensure everything is complete before listing the business for sale.

- Sale Execution (Typically 3–6 Months)

In the final phase, the business is listed for sale, and potential buyers conduct due diligence. Ontario business owners should be prepared for thorough reviews of contracts, financial records, and regulatory compliance. Due diligence alone can take several months, depending on the business’s complexity and buyer interest. A well-organized process with accessible documents can accelerate negotiations and help secure a favourable sale. Once due diligence is complete, finalize the sale with clear terms, ensuring a smooth handover for all parties involved.

Factors Affecting the Timeline

The time required to exit a business in Ontario can vary based on several key factors. Recognizing these variables allows Ontario business owners to tailor their exit strategy to their unique circumstances and avoid potential delays.

- Market Conditions: Favorable market conditions—such as high demand in the industry or economic growth—can speed up the sale, while downturns may prolong the process as buyers become cautious.

- Business Size and Complexity: Larger businesses or those with complex structures generally need more time for preparation and negotiation. The due diligence process, legal reviews, and valuation are often more detailed for these businesses.

- Buyer Financing Options: The timeline can also be influenced by the financing options. Pre-qualified buyers with financing may help streamline the sale, while buyers seeking additional financing may extend the timeline.

Understanding these factors helps Ontario business owners plan their exit with realistic expectations, adjusting the timeline to match their business goals and market conditions.

Frequently Asked Questions

How can early planning impact the success of my business exit?

Early planning enhances your business’s appeal, streamlines operations, and allows you to explore various exit options, such as selling or family succession. It also reduces risks and ensures you have ample time to make informed decisions, ultimately leading to a smoother transition.

What documentation should I prepare for a business sale in Ontario?

Prepare financial statements, tax records, contracts, permits, and compliance documents. Having these records organized not only accelerates due diligence but also reassures buyers of your business’s stability and compliance with Ontario regulations.

How long does a typical business exit process take?

Exit timelines vary but often range from several months to over a year, depending on factors like business complexity, market conditions, and buyer readiness. Starting early allows you to adapt to changing circumstances and complete each step without pressure.

What tax implications should I consider when selling a business in Ontario?

In Ontario, selling a business may involve capital gains tax, which can impact your sale’s net proceeds. Consulting a tax professional early in the process helps you understand potential liabilities, exemptions, and tax-saving strategies to maximize your returns.

Conclusion

In conclusion, developing a well-planned business exit strategy is essential for a smooth, successful transition that maximizes value and protects your interests. Key steps include setting clear goals, accurately valuing your business, preparing legal and financial documents, and understanding the timeline and tax implications.

The information provided above is of a general nature and should not be considered legal advice. Every transaction or circumstance is unique, and obtaining specific legal advice is necessary to address your particular requirements. Therefore, if you have any legal questions, it is recommended that you consult with a lawyer.