A sole proprietorship is a business structure in which a single individual owns, operates, and manages all commercial activities without forming a separate legal entity. The owner of this structure assumes full personal and financial responsibility for the business, reporting all income and expenses on their personal tax return.

Sole proprietorships benefit from a straightforward registration process, allowing the owner to start and run the business quickly with minimal formalities. You can register a sole proprietorship in Ontario by choosing to operate under your personal legal name or a unique business name. The business receives official recognition when registration is complete and can legally operate under the registered name, with a straightforward taxation process for the owner.

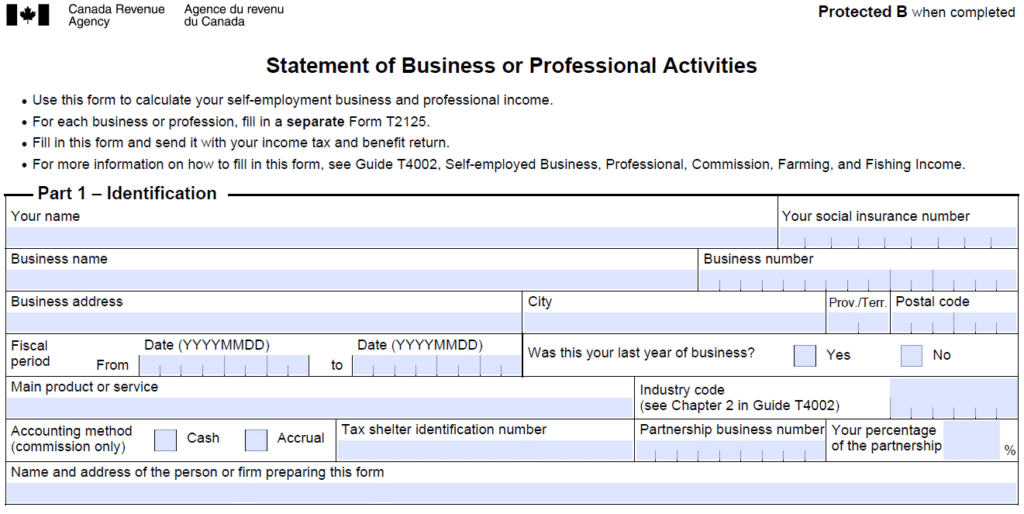

Taxes for a sole proprietorship are reported on the owner’s personal tax return using Form T2125, which records all business income and deductible expenses. The sole proprietor business must comply with federal obligations under the Income Tax Act and provincial requirements in Ontario.

A sole proprietorship offers simple registration, minimal administrative requirements, and full control over business operations. The owners of sole proprietor businesses keep all profits and can make decisions quickly, making it suitable for small businesses and independent professionals. However, the sole proprietors bear unlimited personal liability for business debts and obligations, face limited access to capital, and may experience challenges with business continuity, scaling, or transferring ownership.

If you need assistance from a Toronto corporate lawyer, contact us and see how our firm can help.

What Is Sole Proprietorship?

A sole proprietorship, also known as a sole tradership, individual entrepreneurship or proprietorship, is the simplest and unincorporated business structure wherein a single individual owns and operates the business entirely on their own without creating a separate legal entity. The owner and the business are legally treated as a single entity for legal, tax and liability purposes in this type of business framework.

How to Register a Sole Proprietorship in Ontario?

To register a sole proprietorship in Ontario, decide on a business name, search its availability, register online by providing the required information, pay the registration fee, register for tax purposes, and open a business bank account.

The steps to register a sole proprietorship in Ontario are explained below.

1. Decide Business Name

Decide on a unique business name that represents your sole proprietorship and reflects the activities you intend to carry out in Ontario. You need to decide whether you want to name your business under your legal name or want a different business name. The name of your business in Ontario should not be misleading and confusingly similar to any other registered business or trademark in the province. Your business name must comply with the Ontario Business Names Act. Avoid using restricted words like bank, university, or government in your sole proprietor business name unless you have obtained approval from the relevant provincial or federal authorities in Ontario.

2. Search Name Availability

Search the availability of your chosen business name on the Ontario Business Registry to confirm no other business is using the same or a similar name to avoid disputes with existing businesses and comply with the naming rules set by the Ontario Ministry of Public and Business Service Delivery.

3. Register Online

Register your business name through ServiceOntario’s online portal or by visiting a ServiceOntario centre in Ontario once the business name is confirmed as available. The online business name registration process requires providing the proprietor’s legal details such as your full legal name, residential address, your contact information, the business name, and the primary address of your business operations in Ontario. The ServiceOntarios’s online portal then generates a Master Business Licence which serves as proof of registration and allows your business to operate legally under the chosen name in Ontario.

4. Provide Required Information

Provide the required information during the registration of a sole proprietorship in Ontario which include the business name, owner’s full legal name, residential address, business address, mailing address, and contact information. You must also submit details such as a description of the business activities, the business start date, the expected number of employees, and the owner’s consent and declaration confirming the accuracy of the information provided.

5. Pay the Registration Fee

Pay the required registration fee to complete the sole proprietorship registration process in Ontario. The registration fee is $60 CAD if you register online through ServiceOntario’s online portal and $80 CAD if you submit the registration by mail or in person as set by provincial regulations. Registration fee confirms your application and enables the issuance of the Master Business Licence.

6. Register for Taxes

Register your sole proprietorship for tax purposes by getting a Business Number (BN) from the Canada Revenue Agency (CRA). You need to register for Goods and Services Tax (GST) or Harmonized Sales Tax (HST) if your business earns more than $30,000 CAD in taxable revenue per year which is the provincial threshold for mandatory registration. The process of tax registration requires providing the business number, legal name, and details of business operations to the CRA. Registration for taxes is essential for compliance with federal and provincial tax requirements.

7. Open a Business Bank Account

Open a business bank account once your business is officially established and any required tax registrations are completed in Ontario. It is recommended to keep business transactions separate from personal finances and make expense tracking and accounting easier while a separate account is not legally required for a sole proprietorship. Banks typically require the Master Business Licence, identification, and business details to open the account for sole proprietor business.

Starting a sole proprietorship in Ontario is simple, governed by the Business Names Act and tax laws. While this structure offers flexibility and control, individuals must consider the risks of unlimited personal liability and tax obligations. It is recommended to speak to a corporate lawyer and accountant if you are thinking of starting a sole proprietorship to meet the legal requirements and manage the sole proprietorship effectively.

How to File Taxes for a Sole Proprietorship in Canada?

To file taxes for a sole proprietorship in Canada, the owner completes Form T2125 to report all business income and expenses as part of their personal tax return. They must track all deductible expenses, maintain organized records, meet tax filing deadlines, register for and report GST/HST if required, and remit Canada Pension Plan (CPP) contributions and installments as applicable.

The steps to file taxes for a sole proprietorship in Canada are explained below.

1. Complete Form T2125

Complete Form T2125 (Canadian income tax form) to report your sole proprietorship’s business income, cost of goods sold, and deductible expenses to the Canada Revenue Agency (CRA). You have to provide accurate details of all income earned, expenses incurred, and costs associated with goods sold during the fiscal year while completing the form. Properly filling out Form T2125 makes sure your business comply with CRA requirements and helps avoid audits, penalties, or delays in processing your personal income tax return.

2. Track Expenses

Track all business-related expenses to accurately report deductible costs when filing your personal income tax return and completing Form T2125. Record all operational, administrative, and professional expenses immediately as they are incurred to accurately reflect deductible costs for reporting on Form T2125. Organize receipts, invoices, and bank statements by category and date, and use accounting software or spreadsheets to log each transaction systematically. You should regularly reconcile your expense records with your financial statements to maintain an up-to-date and complete record for tax reporting.

3. Meet Filing Deadlines

Meet filing deadlines by submitting your personal income tax return on or before the dates set by the Canada Revenue Agency (CRA). The Canada Revenue Agency requires the T1 personal income tax return, including Form T2125, to be filed by June 15 for most sole proprietors. Any taxes owed must be paid by April 30 to avoid interest charges. You should plan to efficiently gather all records and financial statements.

4. Register for GST or HST

Register your business for GST and HST if its revenue exceeds $30,000 CAD. Registration requires the sole proprietor to obtain a GST/HST account through the CRA’s Business Number (BN) system. Sole proprietors earning over $30,000 CAD annually must register for GST/HST with the Canada Revenue Agency.

5. Keep Record

Keep record of all financial documents that substantiate income, expenses, and tax reporting of your sole proprietor business. Owners must keep receipts for business purchases and expenses, invoices issued to clients, bank statements, and contracts for a minimum of six years as required by the Canada Revenue Agency. Proper record keeping supports claims made on Form T2125 and GST/HST filings. Organized records reduce administrative burden during audits and protect the owner in case of CRA review or disputes.

6. Calculate CPP Payments

Calculate CPP (Canada Pension Plan) payments based on net business income reported on Form T2125. CPP Contributions are included with your personal income tax filings and help fund retirement benefits. Failure to remit accurate CPP amounts results in penalties or interest charges. Proper CPP calculation guarantees compliance with federal pension obligations and secures future entitlements.

7. Pay Installments

Pay installment payments for income tax and CPP (Canada Pension Plan) contributions on time or as required by the CRA during the tax year. The Canada Revenue Agency (CRA) requires quarterly installment payments when a sole proprietor’s tax payable exceeds the prescribed threshold. Installment amounts are calculated using prior-year tax liability or CRA-issued installment reminders. Making timely installments reduces large balances owing at year-end and prevents interest charges.

What Are the Advantages of Sole Proprietorship?

The advantages of sole proprietorship include simplicity in formation, full managerial control, direct financial benefit and simplified tax filing. It has minimal administrative obligations, simplified banking, and ability to dissolve easily which allows the owner to operate and manage the business efficiently.

The benefits of sole proprietorship are explained below.

Easy and Inexpensive to Form

A sole proprietorship is simple to establish because it does not require incorporation or corporate governance structures. The owner can start sole proprietor business quickly at a lower cost as fewer documents and regulatory filings are needed.

Complete Control and Flexibility

A sole proprietor has complete control and flexibility over operational decisions, contractual commitments, and daily business management. No board of directors, shareholders or partners participate in decision-making or governance of sole proprietor businesses. The owner can change business strategies, services or contractual arrangements without internal approvals. Sole proprietorship allows faster decision-making and quick adjustments in response to market conditions or business priorities.

Simplified Tax Filing

A sole proprietorship does not create a separate corporate taxpayer. Business income is taxed together with the owner’s personal income reporting obligations that removes the requirement for separate corporate income tax filings and helps avoid double taxation that corporations face. This reporting structure of sole proprietorship simplifies the owner’s overall tax compliance process and makes it more straightforward than incorporated business entities.

Keep All Profits

A sole proprietor receives all profits generated by the business after meeting operational obligations and expenses. Profits are not distributed among shareholders or business partners. The owner independently determines how business earnings are allocated or reinvested which provides direct financial benefit from the business’s commercial performance.

Lower Administrative Costs

Sole proprietorship involves fewer corporate compliance requirements than incorporated business structures. This type of business framework does not include shareholder meetings, director resolutions, or corporate minute books to maintain. A sole proprietor manages operations without maintaining extensive corporate documentation that reduces ongoing administrative and regulatory responsibilities which result in lower operational management costs.

Simplified Banking

Banking arrangements for a sole proprietorship are straightforward as financial institutions allow the opening of accounts by using only the owner’s identification and registered business name. Corporate formation documents or shareholder records are unnecessary which reduces the administrative steps required to open a bank account and allows faster access to business banking services. The simplicity of banking arrangements in sole proprietorship allows the owner to focus on operations rather than complex financial procedures.

Easy Dissolution

Dissolving a sole proprietorship is simpler than closing an incorporated business. The owner can discontinue operations at their discretion without shareholder or director approvals because the business and owner are legally the same. They do not require any formal corporate dissolution filings and lengthy procedures. This ease allows the owner to dissolve the business quickly while minimizing administrative obligations.

What Are the Disadvantages of Sole Proprietorship?

The disadvantages of sole proprietorship include personal liability for all business debts, limited access to capital, and full responsibility for daily operations. They also include lack of continuity, challenges in scaling, higher audit exposure, and difficulty transferring ownership.

The disadvantages of sole proprietorship are given below.

Unlimited Liability

Sole proprietors are personally responsible for all business debts, contractual obligations, and legal claims. Creditors can pursue the owner’s personal assets to satisfy liabilities, increasing financial risk in disputes or contractual breaches.

Limited Access to Capital

Sole proprietorships have limited access to capital as they cannot issue stock or bonds, relying on personal savings, loans, or retained earnings for funding. This restricts their growth, limits strategic investments, and constrains competitive positioning compared with incorporated businesses.

Total Responsibility or Burnout

The sole proprietor business owner bears full responsibility for operations, client contracts, and compliance without formal governance support. The cumulative workload can lead to stress and burnout, potentially affecting business performance.

Lack of Continuity

The business exists only through the owner. Events such as illness, retirement, or death disrupt operations, making the sole proprietorship less stable than corporations or partnerships that exist independently of the founder.

Harder to Scale

Expansion of a sole proprietor business is limited by the owner’s resources, capital, and management capacity. Growing operations or services of a proprietor business requires additional investment and planning, constraining long-term business development.

Higher Risk of Audit

The reporting of combined personal and sole proprietor business income increases the likelihood of CRA audits. Errors or omissions in financial records trigger regulatory scrutiny, necessitating detailed accounting and compliance procedures.

No Tax Benefits of Incorporation

Sole proprietorships cannot utilize corporate tax planning strategies such as income splitting or deferred taxation. Business income is reported personally, limiting legal tax mitigation and governance options.

Hard to Transfer Ownership

The sole proprietor business is inseparable from the owner, making transfer of ownership complex. Selling requires individually transferring assets, contracts, and client relationships, which deters buyers or investors and demands detailed legal agreements.

How to Get an HST Number for a Sole Proprietorship?

To get an HST number for a sole proprietorship, you can use different methods like applying online through the CRA’s Business Registration Online (BRO) service, requesting it by phone through the CRA business enquiries line, or submitting the application by mail or fax for processing and confirmation.

Method 1: Online

Apply for an HST number online through the Canada Revenue Agency (CRA) using the Business Registration Online (BRO) service. The online HST registration method allows you to submit your business information electronically and receive confirmation once the registration is completed.

Method 2: By Phone

Request an HST number by contacting the Canada Revenue Agency (CRA) through its business enquiries line. A CRA representative records the required business details and processes the registration during the call.

Method 3: Mail or Fax

Apply for an HST number by completing the appropriate CRA registration form and submitting it by mail or fax. The CRA issues the HST account details and confirms the registration once the application is reviewed.

How to Close a Sole Proprietorship in Ontario?

To close a sole proprietorship in Ontario, the proprietor has to cancel the business name registration, notify the Canada Revenue Agency (CRA), and file final tax returns. The proprietor also needs to cancel licences or permits, settle liabilities, notify stakeholders, and cancel any business-related subscriptions or insurance.

The steps to close a sole proprietorship in Ontario are given below.

1. Cancel Business Name Registration

Cancel the registered business name through the Ontario Business Registry by providing identification and Master Business Licence details, signaling that the sole proprietorship will no longer operate under that name.

2. Notify the CRA

Inform the Canada Revenue Agency (CRA) that the sole proprietorship has ceased operations, providing the business number and closure date so the CRA can update accounts and close business-related tax records.

3. File Final Tax Returns

Submit final tax returns of your business to report income and expenses up to the closure date, ensuring the CRA has a complete record of the business’s final reporting period.

4. Cancel Licences or Permits

Terminate all sole proprietor business licences and permits by notifying the issuing municipal or provincial authorities, providing the business name, licence details, and confirmation of closure.

5. Settle Liabilities

Resolve all outstanding debts, contractual obligations, supplier arrangements, and other business-related liabilities before completing the closure process.

6. Notify Stakeholders

Communicate the closure of your sole proprietor business to clients, suppliers, service providers, and other relevant parties to ensure agreements and service arrangements are properly concluded.

7. Cancel Subscriptions or Insurance

End all subscriptions and insurance policies linked to your sole proprietor business by contacting providers, providing business details, and confirming the cessation of operations.

What Are the Liability Risks for Sole Proprietors?

The liability risks for sole proprietors are full personal responsibility for all business debts, contractual obligations, and legal claims. Sole Proprietors will have to use personal assets to cover expenses, damages, or losses arising from business operations and have limited legal protection because their businesses are not separate from the owner.

The liability risks for sole proprietorship are given below.

- Unlimited Personal Liability: Sole proprietors are fully personally liable for all business debts and obligations, putting their personal assets, such as savings, property, and investments, at risk if the business cannot meet financial obligations.

- Lawsuits and Damages: Legal claims arising from negligence, contractual disputes, or service failures directly expose the sole proprietor to personal financial responsibility for any awarded damages.

- Contractual Debt: Debts from business contracts, including loans, supplier agreements, or leases, create a risk of personal liability if the proprietor fails to fulfill the contractual obligations.

- Business Interruption: Unexpected events, like equipment failure, supply chain disruptions, or litigation delays, can generate ongoing costs that the sole proprietors must cover personally, increasing financial vulnerability.

- Limited Protection: The lack of legal separation between the owner and the business leaves sole proprietors exposed to claims from creditors, clients, or third parties without the liability shield that incorporation provides.

What Is the Difference Between Sole Proprietorship and Corporation?

The main difference between a sole proprietorship and a corporation in Ontario is liability. A sole proprietor is personally responsible for all business debts while a corporation limits personal liability by creating a separate legal entity. A sole proprietorship reports business income on the proprietor’s personal tax return whereas a corporation files its own corporate tax return under corporate tax rules. Establishing a sole proprietorship is simpler and less costly while incorporating a business requires formal documentation, compliance with corporate governance, and higher fees.

You should consider factors such as personal liability protection, long-term growth plans, and administrative requirements when choosing between a sole proprietorship and a corporation. Consult with a legal professional to determine the most suitable structure based on your business’s objectives and operational needs in Ontario.

Frequently Asked Questions

Can I Change My Sole Proprietorship to a Corporation in Ontario?

Yes, you can change your sole proprietorship to a corporation in Ontario by formally incorporating the business under the Ontario Business Corporations Act. This process involves preparing and filing incorporation documents, selecting a corporate name, and creating the necessary corporate structure including shareholders, directors and officers. The assets, contracts, and operations of the sole proprietorship are transferred to the new corporate entity through proper legal agreements once the corporation is established.

Why Do People Prefer Sole Proprietorship?

People prefer a sole proprietorship because it is less complex and less expensive to establish than incorporated business structures. It is also versatile and accessible which allows individuals to operate independently and manage their services directly without extensive governance requirements or corporate formalities.

What Is an Example of Sole Proprietorship?

Examples of sole proprietorship include freelance consultants, writers, independent contractors, trainers, small retail shop owners, tutors, and self-employed tradespeople such as electricians, housekeepers or graphic designers.

When to Choose Sole Proprietorship?

A sole proprietorship is chosen when you want a simple, low‑cost, and informal business structure with minimal regulatory requirements. This structure works well for independent operators and freelancers who want to retain full control and report business income directly on their own tax return without creating a separate legal entity. It is particularly suitable when you are just beginning your business, managing limited financial risk, or operating part‑time before considering more complex structures like incorporation.

Can a Sole Proprietorship Hire Employees?

Yes, a sole proprietorship can hire employees in Ontario provided the sole proprietor complies with federal and provincial employment laws. Sole proprietors must register with the Canada Revenue Agency (CRA) as an employer and set up payroll accounts. A sole proprietor is required to deduct contributions such as Canada Pension Plan (CPP) premiums and Employment Insurance (EI) premiums. Sole proprietors are responsible for maintaining a safe workplace, adhering to minimum wage and labour standards, and keeping accurate employment records.

Can Sole Proprietors Pay Themselves a Salary?

No, sole proprietors cannot pay themselves a salary in the formal sense because the business is not a separate legal entity from the owner. The owner takes an owner’s draw by withdrawing business profits directly for personal use instead of a salary and all net profit is reported as personal income for tax purposes. These withdrawals are not considered payroll and do not require payroll deductions like Canada Pension Plan (CPP) or Employment Insurance (EI).

Can I Use My Personal Bank Account to Run a Sole Proprietorship?

Yes, you can use your personal bank account to run a sole proprietorship because the business is not legally separate from the owner. It is better to use a separate business account to clearly distinguish personal and business transactions for accounting and tax reporting. Mixing funds makes it difficult to track income, document deductible expenses, and support records during a Canada Revenue Agency (CRA) review. A separate account is required when registering for GST/HST or when financial institutions require a business account for certain commercial transactions.

Can a Sole Proprietorship Have Two Owners?

No, a sole proprietorship cannot have two owners because it is legally owned and operated by a single individual. A sole proprietor is an individual proprietor who has full responsibility for the business including all debts, obligations, and decision-making authority. A sole proprietorship structure allows the proprietor to maintain complete control over all business operations.

Do I Need to Register a Sole Proprietorship?

Yes, you need to register a sole proprietorship depending on whether the business operates under the owner’s legal name or a different business name. Businesses using a name other than the proprietor’s personal legal name must register with the Ontario Business Registry to operate legally. Registration of a sole proprietorship provides recognition in commercial dealings and allows the proprietor to open a business bank account. It supports proper structuring of contracts, agreements, and potential dispute resolution.

Do I Need an HST Number For a Sole Proprietorship?

No, a sole proprietorship does not require a Harmonized Sales Tax (HST) number in Canada, as it depends on the business’s annual revenue. Businesses with revenue below $30,000 are considered small suppliers and are not required to register for HST. Sole proprietors expecting to exceed the $30,000 threshold or wishing to claim input tax credits can register voluntarily.

Does a Sole Proprietor Need a Business Licence in Ontario?

Yes, a sole proprietor needs a business licence or registration in Ontario when the business operates with employees, facilities, or offices in Ontario. The business must register through the Ontario Business Registry to operate under a business name. Sole proprietors do not need licences or permits for some businesses like accounting offices, consulting services, graphic design services, writing services, and catering services that do not serve the public.

Is There a Limit to My Earnings as a Sole Proprietor?

No, there is no legal limit to your earnings as a sole proprietor in Canada. Sole proprietor has unlimited liability, holds full responsibility for all business decisions, receive all profits generated by the business, and can claim any financial losses as part of their business activities. The maximum allowable profit is not capped, so your earnings are entirely determined by the business’s performance.

The information provided above is of a general nature and should not be considered legal advice. Every transaction or circumstance is unique, and obtaining specific legal advice is necessary to address your particular requirements. Therefore, if you have any legal questions, it is recommended that you consult with a lawyer.