A Section 85 rollover is a tax-deferred transfer mechanism under the Income Tax Act (R.S.C., 1985, c. 1 (5th Supp.)) that permits a taxpayer to elect to transfer eligible property to a taxable Canadian corporation without triggering immediate tax consequences. Its purpose is to defer the recognition of capital gains or other income and to facilitate incorporation, corporate reorganizations, and estate planning strategies. A Section 85 rollover requires the transferor and transferee to agree on an elected amount for each property, which becomes the transferor’s proceeds of disposition and the corporation’s cost of the property. Eligible property under Section 85 includes capital property, inventory, depreciable property, eligible intangible property, and shares or debt of other corporations, subject to statutory limitations.

A taxpayer may elect under Section 85 of the Income Tax Act to transfer eligible business property to a taxable Canadian corporation on a tax-deferred basis. To comply with Section 85 of the Income Tax Act, the taxpayer and the corporation must jointly file Form T2057 with the Canada Revenue Agency, supported by proper documentation. Completing a valid Section 85 election allows taxpayers to defer tax, facilitate incorporation, implement estate freezes, structure consideration flexibly, undertake corporate reorganizations, and control the elected amount within permissible limits. These features make a Section 85 rollover a widely used mechanism for transferring appreciated property, establishing holding companies, carrying out corporate reorganizations, and implementing succession planning strategies.

Many Canadian business owners use a Section 85 rollover to transfer assets to a corporation while deferring taxes, but the rules under the Income Tax Act can be complex to understand. A business lawyer can help make sure the elected amounts are accurate, the required forms are properly filed, and the transaction is structured to maximize tax deferral and compliance.

What Is Section 85 Rollover?

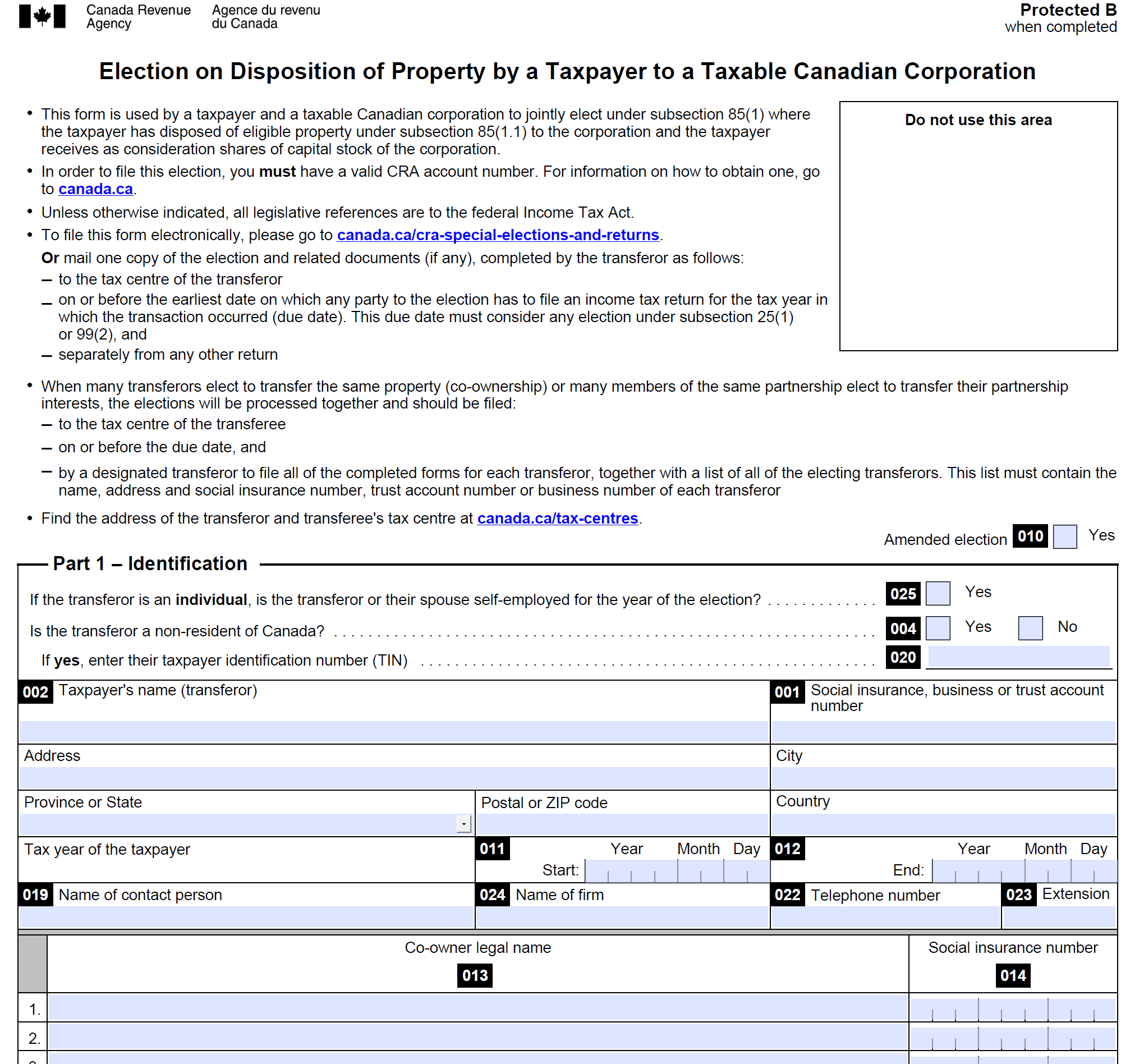

A Section 85 rollover is a tax-deferred election under the Income Tax Act (R.S.C., 1985, c. 1 (5th Supp.)) that allows a taxpayer to transfer eligible assets to a corporation without triggering immediate capital gains or recapture taxes. A mandatory requirement of Section 85 rollover is that it must be a joint election made by both the transferor and the transferee. The transfer of eligible assets to a corporation under a Section 85 rollover must be reported to the Canada Revenue Agency (CRA) using Form T2057, the prescribed form under Section 85 of the Income Tax Act. A Section 85(1) rollover allows a taxpayer, including a sole proprietorship, to transfer eligible business assets to a corporation while deferring capital gains taxes and facilitating business incorporation.

How Does Section 85 Rollover Work?

A Section 85 rollover allows a taxpayer to transfer eligible property (including business assets and shares) to a taxable Canadian corporation on a tax-deferred basis under the Income Tax Act. The transferor and the corporation must jointly file Form T2057 with the Canada Revenue Agency and agree on an elected amount for each property, which becomes the transferor’s proceeds of disposition and the corporation’s cost of the property.

The elected amount must fall within prescribed limits, generally between the adjusted cost base (ACB) or undepreciated capital cost (UCC) and the fair market value of the property. The elected amount determines the extent of tax deferral: an amount set near the tax cost generally defers gains, while a higher elected amount may result in partial gain recognition.

The corporation must issue at least one share as consideration, and any non-share consideration (“boot”), such as cash or other property, may trigger immediate tax consequences, including capital gains or recapture of depreciation, depending on the nature of the property and the elected amount. Accordingly, a Section 85 rollover defers, in whole or in part, the recognition of gains until a future disposition of the property by the corporation or a disposition of the shares by the transferor.

When Should You Use a Section 85 Rollover?

You should use a Section 85 rollover when incorporating a business, transferring appreciated assets, estate planning, business reorganization, or setting up a holding company. It allows eligible assets to be transferred to a corporation while deferring capital gains tax and establishing a structured cost base.

The uses of Section 85 rollover are provided below.

- Incorporation of a Business: A Section 85 rollover allows business assets to be transferred to a newly incorporated corporation while deferring taxes and preserving capital for growth.

- Transferring Appreciated Assets: The Section 85 rollover allows appreciated property to move into a corporation without triggering immediate capital gains tax to help retain value for the business.

- Estate Planning and Family Planning: Section 85 rollover can be used to transfer assets as part of succession planning, freezing their value for estate purposes, and potentially reducing taxes for heirs.

- Business Reorganization: The Section 85 rollover allows assets to be moved between corporations during mergers, amalgamations, or restructurings without triggering immediate tax, which maintains the value of business assets.

- Setting Up a Holding Company: Section 85 rollover can be used to transfer assets to a holding company, to centralize ownership and create a tax-efficient structure for future investments or distributions.

What Ontario-Specific Considerations Apply to a Section 85 Rollover?

While Section 85 of the Income Tax Act is a federal provision, transactions involving Ontario taxpayers or assets may give rise to additional provincial legal and tax considerations depending on the specific facts and structure of the rollover.

Ontario Land Transfer Tax (LTT)

The transfer of real property situated in Ontario as part of a Section 85 rollover may be subject to land transfer tax under the Land Transfer Tax Act. Section 85 does not provide a deferral of land transfer tax, as the deferral applies only to income tax under the Income Tax Act.

In addition, transfers of real property located within the City of Toronto may also be subject to Municipal Land Transfer Tax under the City of Toronto Act, 2006.

Certain exemptions or relief provisions may be available under the Land Transfer Tax Act, including in limited circumstances involving transfers between affiliated corporations; however, the availability and applicability of such exemptions depend on the specific facts and should be confirmed with a lawyer.

Corporate Law Compliance (OBCA)

Where the transferee corporation is incorporated under the Ontario Business Corporations Act (“OBCA”), any shares issued as consideration must comply with applicable corporate law requirements. These include rules relating to stated capital, adequacy of consideration, directors’ approvals, and proper corporate authorization.

Ontario Corporate Tax Considerations

Ontario imposes its own corporate income tax regime under the Taxation Act, 2007, which operates alongside the federal system. Tax attributes arising from a Section 85 rollover—such as adjusted cost base, paid-up capital, and elected amounts—may affect Ontario corporate tax calculations, including future distributions and tax liabilities. The specific implications of these attributes should be reviewed in the context of Ontario tax rules.

An Ontario business lawyer can assess whether a proposed Section 85 rollover structure complies with both federal tax rules and Ontario-specific legal requirements.

What Are the Requirements for a Section 85 Rollover?

The requirements for a Section 85 rollover include an eligible transferor, an eligible transferee, eligible property, an election agreement, and an elected amount. They also include timing and deadlines, consideration, boot limitation, legal and tax advice, joint election, and proper documentation.

The important requirements for Section 85 rollover are explained below.

- Eligible Transferor: A Section 85 rollover requires the transferor to be a taxpayer, such as an individual, trust, corporation, or partnership, who owns the property and has the authority to transfer it.

- Eligible Transferee: The transferee must be a taxable Canadian corporation, as required under Section 85 rollover, and must be able to issue shares as part of the transaction.

- Eligible Property: Section 85 rollover applies to capital property, inventory, depreciable assets, and certain intangible assets, as only these eligible property types qualify for tax-deferred transfer under the Income Tax Act.

- Joint Election: The transferor and the transferee must file a joint election using Form T2057 to defer the tax consequences of the transfer and complete a Section 85 rollover.

- Elected Amount: Each asset transferred under Section 85 rollover must have an elected amount, which sets the transferor’s proceeds and the corporation’s cost, within limits such as adjusted cost base (ACB) and fair market value (FMV).

- Timing and Deadlines: The Section 85 rollover election must be filed by the earliest tax filing due date among the transferor and the transferee for the taxation year in which the transfer occurs to secure tax deferral and make sure CRA recognizes the election, although late filings may be accepted under specific CRA rules.

- Consideration: A Section 85 rollover requires the transferor to receive at least one share to qualify for tax deferral, while any additional cash or property (“boot”) is taxable as it represents immediate value received.

- Boot Limitation: The elected amount under Section 85 rollover cannot be less than the fair market value of any boot received to prevent taxpayers from receiving cash or other benefits tax-free.

- Documentation: Proper records, including valuations and tax cost details, should be maintained for a Section 85 rollover to support the election if reviewed by the Canada Revenue Agency.

Who Is an Eligible Transferor Under Section 85?

An eligible transferor under Section 85 includes tax payer individual, a trust, and a corporation that transfers eligible property to a taxable Canadian corporation and jointly elects to apply the rollover provisions. Non-resident transferors are subject to restrictions, as the Section 85 rollover generally applies only to certain types of taxable Canadian property. Partnerships may also qualify as transferors; however, each partner jointly makes the election with the corporation using Form T2058, and the tax consequences flow through to the partners in accordance with partnership rules. Lawyer verification is recommended to confirm the precise mechanics under Section 85(2).

Who Is an Eligible Transferee Under Section 85?

An eligible transferee under Section 85 of the Income Tax Act is a taxable Canadian corporation that receives eligible property from a transferor and participates in a joint election. The corporation must issue shares of its capital stock to the transferor as part of the consideration for the transferred property, which is required for the rollover to qualify. This requirement makes sure that the corporation remains subject to Canadian tax on any future disposition of the property.

What Is Eligible Property Under Section 85?

The eligible property under Section 85 is tangible personal property, real property, intangible assets, inventory, capital property, shares, and debt of other corporations.

The types of eligible property under Section 85 are provided below.

- Tangible Personal Property: Section 85 allows the transfer of tangible assets such as machinery, vehicles, and equipment used in business operations.

- Real Property: Land and buildings can be transferred under Section 85, including commercial real estate like offices, manufacturing facilities, retail spaces, and investment properties.

- Inventory: Businesses may transfer inventory under Section 85 without triggering immediate tax, including goods held for sale in manufacturing, retail, or wholesale operations.

- Depreciable Property (including Class 14.1 property such as goodwill, customer lists, patents, and trademarks): Certain intangible assets formerly classified as eligible capital property are now Class 14.1 depreciable property under the Income Tax Act. These assets remain eligible for transfer under Section 85, even though they do not have a fixed lifespan.

- Shares and Debt of Other Corporations: Section 85 permits the transfer of eligible shares or debt of other corporations to support corporate restructuring and consolidation of business interests.

What Is the Cost of Consideration in a Section 85 Rollover?

Cost of consideration in a Section 85 rollover is the value assigned to the property received by the transferor in exchange for the assets transferred to the transferee corporation. It is calculated based on the agreed or elected amount, which must fall between the asset’s adjusted cost base (ACB) and its fair market value (FMV) at the time of transfer, establishing the total cost base for tax purposes.

Consideration received by the transferor may include shares of the transferee corporation and non-share consideration (boot), such as cash or other property. Shares allow for tax deferral, while boot can trigger immediate tax consequences, including capital gains or recapture, depending on the elected amount and the nature of the property. Structuring the cost consideration carefully allows the transferor to achieve tax deferral, minimize immediate capital gains or recapture, and comply with the Income Tax Act (ITA), while providing the corporation a proper cost base for future tax planning and depreciation.

How to File CRA Form T2057 for a Section 85 Rollover?

To file CRA Form T2057 for a Section 85 rollover, you must download and complete the form, inventory your business assets, obtain fair market valuations, determine elected amounts, structure share consideration, submit the form within deadlines, and update corporate records. Filing Form T2057 for a Section 85 rollover involves detailed reporting requirements, accurate valuations, and strict compliance with CRA deadlines. You can hire a corporate lawyer to guide you through the entire process, so all documentation is accurate, deadlines are met, and the election complies with the Income Tax Act.

To file CRA form T2057, follow the steps given below.

- Download and Complete Form T2057: Obtain the latest version of Form T2057 from the CRA website and fill in all required Sections, including transferor, transferee, and property details, to formalize the Section 85 rollover election.

- Inventory Your Business Assets: List all eligible properties to be transferred under the Section 85 rollover, so each asset is clearly described and grouped if necessary.

- Obtain Fair Market Valuations: Determine the fair market value of each asset at the time of transfer to establish limits for the elected amount and support compliance with Section 85 rollover rules.

- Determine Elected Amounts: Set the elected amount for each property in a Section 85 rollover to establish the transferor’s proceeds and the corporation’s cost, ensuring it stays between the asset’s adjusted cost base (ACB) and fair market value (FMV).

- Structure Share Consideration: Decide the number and type of shares, and any non-share consideration (boot), to be issued by the transferee corporation as payment for the transferred assets, so the transaction qualifies for the Section 85 rollover.

- Submit Form Within Deadlines: File the completed T2057 with the Canada Revenue Agency (CRA) tax centre by the earliest tax filing date for the transfer year to validate the Section 85 rollover election.

- Update Corporate Records: Document the asset transfers, issued shares, and elected amounts in the corporation’s accounting and legal records to properly track the Section 85 rollover.

What Are the Advantages of a Section 85 Rollover?

The advantages of a Section 85 rollover include significant tax deferral, incorporation efficiency, estate planning and freezes, flexibility in consideration, corporate restructuring, and flexibility in elected amount.

The advantages of the Section 85 rollover are explained below.

- Significant Tax Deferral: The Section 85 rollover reduces immediate tax liabilities by allowing the transferor to defer capital gains or recapture taxes that would otherwise arise on the disposition of assets.

- Incorporation Efficiency: Section 85 rollover transfers assets to a newly incorporated or existing corporation, simplifying the process of setting up or reorganizing a business.

- Estate Planning and Freezes: The Section 85 rollover enables strategic estate planning by freezing the value of transferred assets and reducing future taxes for heirs or beneficiaries.

- Flexibility in Consideration: Section 85 rollover allows transferors to receive shares, non-share consideration (boot), or a combination, which allows for tailored structuring to meet financial and tax planning goals.

- Corporate Restructuring: Section 85 rollover facilitates mergers, reorganizations, or the consolidation of multiple business assets under a single corporate entity without immediate tax consequences.

- Flexibility in Elected Amount: The agreed-upon elected amount in a Section 85 rollover can be set within allowable limits to optimize tax outcomes, including partial recognition of gains when advantageous.

Frequently Asked Questions

What Is the Difference Between Section 85 and 86 Rollovers?

The difference between Section 85 and Section 86 rollovers is primarily in their applications, eligible property, scope, process and procedural mechanism, flexibility and control, estate freezes, boot consideration, and transaction requirements.

The table below gives a clear comparison between Sections 85 and 86 rollover.

| Criteria | Section 85 Rollover | Section 86 Share Exchange |

| Applications | Transfers assets into a corporation tax-deferred; used for incorporation, holdco structures, or business transfers. | Reclassifies or exchanges shares within a corporation; used for internal reorganizations and estate freezes. |

| Eligible Property | Business assets, capital property, inventory, intangible assets, and certain shares must go to a taxable Canadian corporation. | Shares of a corporation allow the exchange of one class for another without immediate tax. |

| Process | Requires joint election using Form T2057 (or T2058 for partnerships) and agreement on elected amounts. | No prescribed CRA election form is required, but the reorganization must meet the conditions set out in the Income Tax Act for rollover treatment to apply. Lawyer verification recommended. |

| Flexibility | High flexibility allows the elected amount, consideration (shares or boot), and timing to be chosen. | Limited flexibility means share exchange terms are fixed by Income Tax Act rules. |

| Estate Freezes | Possible but less common; can fix asset value in corporate transfers. | Commonly used to convert existing shares to preferred shares and issue new growth shares to heirs. |

| Boot | Allowed, affects the elected amount, and must comply with limits. | Non-share consideration (boot) is permitted under Section 86; it affects the adjusted cost base of the shares received and may trigger gain recognition. Lawyer verification recommended. |

| Requirements | Joint election, documentation, CRA filing, and professional advice recommended. | Must comply with Income Tax Act share reorganization rules; CRA filing usually not required. |

Can I Rollover My Capital Gains Into Another Property?

No, you cannot rollover capital gains into another property tax-free, because Section 85 only allows deferral of gains when transferring eligible property to a taxable Canadian corporation. The transferor and corporation must jointly elect an elected amount on CRA Form T2057, the corporation must issue at least one share, and any non-share consideration (“boot”) can trigger immediate tax. Section 85 cannot be used for personal reinvestment, though limited deferral may be possible under replacement property rules with strict conditions.

How Section 85 Rollover Works for Small Business Owners?

Section 85 rollover works for small business owners by allowing sole proprietors to transfer eligible business assets to a taxable Canadian corporation without immediate tax consequences, deferring capital gains until a future disposition. This process involves identifying eligible assets, determining the elected amount for each, and jointly filing Form T2057 with the CRA. The transferor must receive at least one share in the corporation as part of the consideration, and once completed, the business assets move into the corporation while preserving tax-deferred status.

How Can Small Business Owners Elect for Section 85 Rollover?

Small business owners can elect for a Section 85 rollover by following the steps given below.

- Incorporate & Identify Assets: Establish a taxable Canadian corporation and list all eligible business assets, such as tangible property, inventory, or intangible assets, intended for transfer under Section 85.

- Determine Elected Amount: Set the elected amount for each asset in a Section 85 rollover between ACB/UCC and FMV, and not below the FMV of any boot.

- Draft Purchase & Sale Agreement: Prepare a purchase and sale agreement for the Section 85 rollover detailing the transferred assets, consideration, and elected amounts for clear documentation and CRA compliance.

- Complete Form T2057: Fill out Form T2057 with details including details of each property, elected amounts, and consideration received, to complete the Section 85 election.

- File within Deadlines: Submit Form T2057 to the Canadian Revenue Agency by the transferor’s earliest tax filing due date to preserve Section 85 deferral. The CRA may allow late filings, but penalties or discretionary relief can apply.

- Receive Shares or Consideration: Make sure the transferor obtains at least one share (or fraction of a share) from the corporation, with any additional non-share consideration properly documented to satisfy Section 85 requirements.

Electing for a Section 85 Rollover as a small business owner requires careful planning, including identifying eligible assets, setting elected amounts, drafting agreements, and filing Form T2057 on time. You can avoid these issues by hiring a small business lawyer who can provide expert guidance so the election is properly structured, all legal requirements are met, and tax deferral benefits are maximized.

Does a Section 85 Rollover Avoid Ontario Land Transfer Tax?

No. A Section 85 rollover under the Income Tax Act does not provide relief from Ontario land transfer tax. If real property is transferred, land transfer tax may apply under the Land Transfer Tax Act, unless a specific exemption or planning structure is available.

When Does Ontario Land Transfer Tax Apply in a Section 85 Rollover?

Ontario land transfer tax generally applies when a beneficial interest in real property is conveyed to a corporation as part of a Section 85 rollover. The tax is calculated based on the value of the consideration or fair market value, depending on the structure of the transaction.

Do Shares Issuance in a Section 85 Rollover Need to Comply with Ontario Corporate Law?

Yes. If the corporation is incorporated under the Business Corporations Act, any shares issued as consideration must comply with corporate law requirements, including proper authorization, adequacy of consideration, and maintenance of stated capital accounts.

How Does A Section 85 Rollover Affect Ontario Corporate Taxes?

While Section 85 is governed by federal law, Ontario generally follows federal income tax treatment. However, provincial corporate tax calculations, including income allocation and future distributions, may be impacted by the tax attributes established through the rollover.

Can Real Estate Be Transferred to A Corporation in Ontario Using a Section 85 Rollover?

Yes. Real estate located in Ontario can be transferred to a taxable Canadian corporation under Section 85. However, such transfers may trigger Ontario land transfer tax and require proper legal documentation, registration, and valuation.

Is Legal Documentation Required for A Section 85 Rollover Involving Ontario Assets?

Yes. In addition to filing Form T2057 with the Canada Revenue Agency, transactions involving Ontario assets may require legal agreements, property transfer documents, and corporate resolutions to comply with both federal and Ontario legal requirements.

Do Section 85 Rollovers Require Registration of Property Transfers in Ontario?

Yes. If the rollover involves real property in Ontario, the transfer must be registered through the provincial land registry system, and applicable land transfer tax filings must be completed in accordance with Ontario law.

The information provided above is of a general nature and should not be considered legal advice. Every transaction or circumstance is unique, and obtaining specific legal advice is necessary to address your particular requirements. Therefore, if you have any legal questions, it is recommended that you consult with a lawyer.