Estate planning in Ontario is making arrangements for what happens to your assets during your lifetime and after you pass away. In Ontario this includes various legal documents and strategies such as wills, trusts, powers of attorney and joint ownership. These are to make sure your assets are distributed according to your wishes and minimize taxes and legal headaches. Here’s an overview of estate planning in Ontario, what it’s about and the key components and considerations.

- What Is Estate Planning?

- The Importance of Estate Planning

- Key Components of an Estate Plan in Ontario

- Who Needs Estate Planning?

- Who Can Do Estate Planning?

- What Laws are Applicable for Estate Planning in Ontario?

- Considerations for Estate Planning

- Key Considerations While Choosing an Executor For Your Will

- Minimizing Probate Involvement

- Digital Estate Planning & Social Media: 7 Key Considerations

- Business Owner Consideration – Do Business Owners Need Estate Planning?

- Summary

What Is Estate Planning?

Estate planning is a process of preparing for the management and disposal of an individual’s estate during their lifetime and after they pass away. Depending on the situation it may include drafting a will, powers of attorney for health care and financial decisions, creating trusts and planning for tax implications so assets are distributed according to the individual’s wishes and minimize legal headaches and taxes. The goal is to safeguard one’s legacy, provide for loved ones, and make clear arrangements for end-of-life care and asset distribution. This proactive approach requires consideration of legal, financial and personal details and often requires the guidance of professionals to navigate the complexities of estate laws and regulations.

The main purpose of proper estate planning is to provide clear instructions for what happens to an individual’s estate. This reduces uncertainty and conflict among family members by saying who gets what and when, and it prevents the often messy and lengthy probate process that occurs when someone dies without a will. Also, estate planning allows individuals to make important decisions about their health care and end-of-life care through living wills and health care proxies. So their wishes are respected and loved ones aren’t forced to make tough decisions during emotional times.

Additionally, estate planning strategies can provide significant tax benefits for individuals during their lifetime and their beneficiaries after they pass away. By using trusts, gifting strategies and other financial tools, individuals can minimize estate taxes and increase the value of the estate left to their heirs. Estate planning is not a one time event but an ongoing process that should be reviewed and revised with life events such as marriage, divorce, the birth of children or changes in financial situation. Working with legal and financial professionals who specialize in estate planning is key. They can help navigate the complexities of the laws and regulations and make sure your estate plan reflects your wishes and takes care of your loved ones’ future.

The Importance of Estate Planning

Estate planning is more than just making a will. It’s a holistic approach to your financial health, protecting your assets and your family’s future. In Ontario, without a proper estate plan and the right legal documents, your assets could be distributed according to the province’s laws of intestacy and not according to your wishes. Additionally, inadequate estate planning can mean unnecessary legal fees, taxes, and family conflicts. An estate plan gives you peace of mind, knowing your loved ones are taken care of, and your affairs are in order.

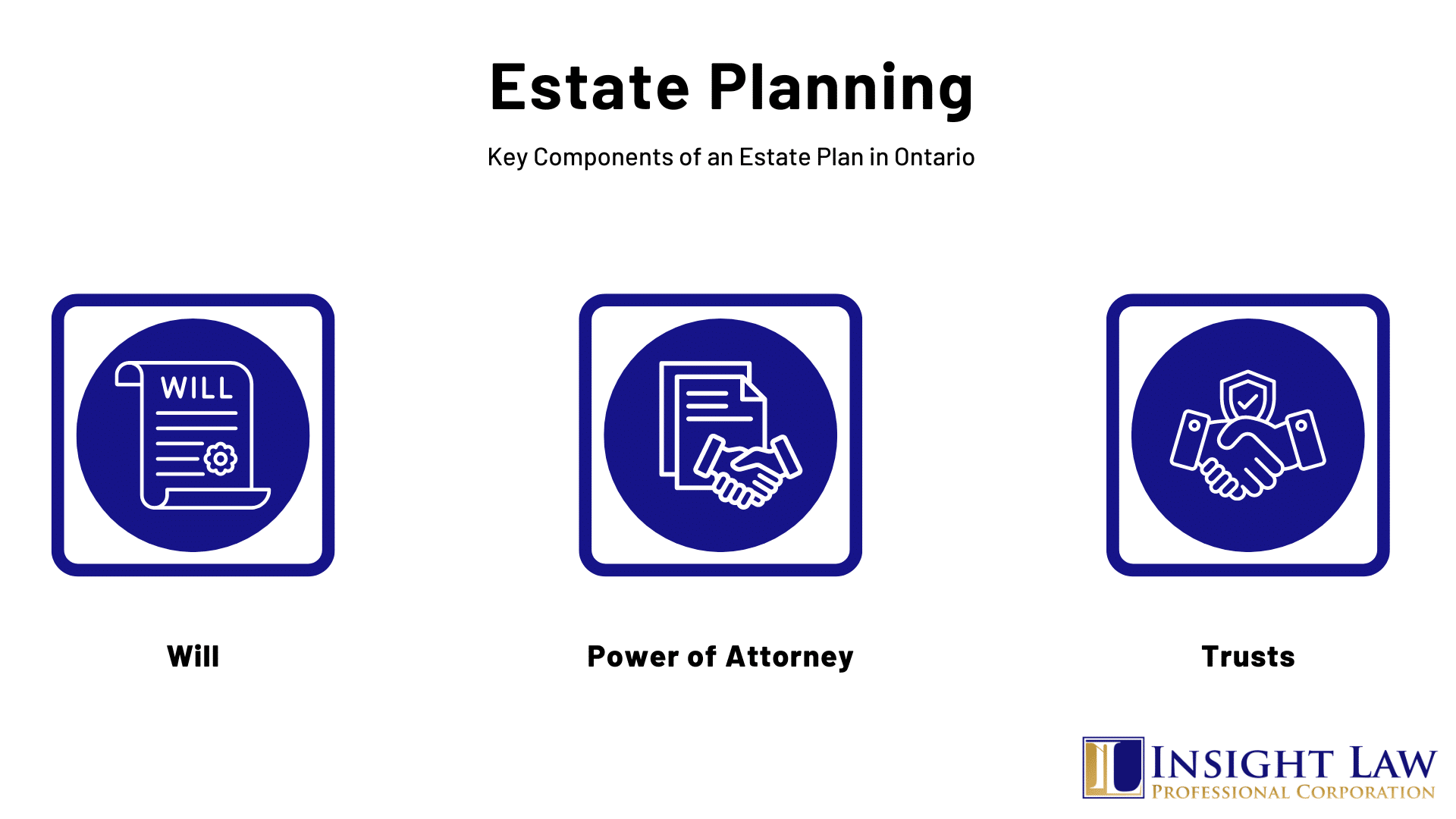

Key Components of an Estate Plan in Ontario

Will

A Will, also known as a Last Will and Testament, is a legal document that outlines a person’s wishes regarding the distribution of their assets and the management of their estate upon their death. It is one of the most common and straightforward tools in estate planning.

A Will specifies how a person’s assets, such as property, bank accounts, investments, and personal belongings, should be distributed among beneficiaries, including family members, friends, or charitable organizations. It also allows the appointment of an executor responsible for executing the wishes outlined in the Will.

Powers of Attorney

Ontario recognizes two types: one for property and another for personal care. These documents allow you to appoint someone to make decisions on your behalf should you become unable to do so due to illness or incapacity. A Power of Attorney for Property covers financial affairs, while a Power of Attorney for Personal Care deals with health care and other personal decisions.

Trusts

A Trust is a legal arrangement in which a person (the grantor or settlor) transfers assets to a Trustee, who manages them. The trustee holds and administers the assets on behalf of the beneficiaries according to the terms specified in the Trust document.

Trusts serve various purposes, such as asset protection, estate tax planning, and ensuring the efficient distribution of assets. Unlike Wills, Trusts can be used to manage assets during the grantor’s lifetime and after death.

Who Needs Estate Planning?

Estate planning is often thought to be only for the rich or old. But the truth is anyone with assets, no matter how big or small, or anyone who wants to have control over their financial and health decisions if they become incapacitated needs estate planning. This includes adults of all ages, from young professionals just starting out to retirees with complex financial situations. Estate planning isn’t just about what happens after you die; it’s about who will manage your finances, make health care decisions for you if you can’t, and make sure minor children are cared for. The myth that estate planning is only for the wealthy ignores the main point of making sure your wishes are respected and your loved ones are taken care of as best as possible.

Plus estate planning can help you avoid the headaches and delays of the probate process, reduce or eliminate estate taxes and minimize family squabbles. For business owners it’s about the smooth transition of the business, so it can continue to operate or be sold according to your wishes. Similarly, people with specific healthcare wishes or wanting to make charitable donations part of their legacy will find estate planning indispensable. In short, estate planning is about taking control of your financial and personal affairs to bring clarity, security and peace of mind to yourself and those you love. It’s a responsible thing to do for anyone who wants to get their affairs in order, no matter what age, wealth or health status.

Who Can Do Estate Planning?

Estate planning often involves working with professionals to make sure all the legal requirements are met and the plan addresses your wishes and needs. Estate lawyers can help with drafting wills, powers of attorney and trusts. Financial advisors can advise on tax implications and asset management strategies to preserve and grow the estate for the beneficiaries. Many people work with tax professionals to navigate the estate and inheritance taxes. No matter how complex your financial situation or family dynamics, working with these professionals will ensure the estate plan is comprehensive, legally sound and tailored to your specific situation and goals.

What Laws are Applicable to Estate Planning in Ontario?

For estate planning in Ontario, Canada, several specific laws govern how individuals can plan for the distribution of their assets, make arrangements for incapacity, and outline their wishes for end-of-life care. Here are some of the many key statutes applicable to estate planning in Ontario:

- Succession Law Reform Act (SLRA): This act is central to estate planning in Ontario, as it governs wills and the distribution of estates. It outlines the requirements for a valid will, rules for intestate succession (when someone dies without a will), and provisions for dependant’s relief, which can affect how an estate is distributed.

- Estates Act: This act provides for the administration of estates in Ontario, detailing the appointment and duties of estate executors and administrators. It covers aspects such as the issuance of probate (now officially called a Certificate of Appointment of Estate Trustee) and the management and distribution of the deceased’s assets.

- Substitute Decisions Act: This act is critical for planning in case of incapacity. It governs appointing powers of attorney for property and personal care, detailing how these legal documents should be executed and the scope of authority they can grant. This allows individuals to designate someone to manage their financial affairs and make health care decisions on their behalf if they cannot do so themselves.

- Trustee Act: This act provides the legal framework for the duties and powers of trustees in Ontario, which is relevant for any estate plan that involves the creation of trusts. It covers the investment of trust assets, the administration of trusts, and the responsibilities of trustees to beneficiaries.

- Income Tax Act (Canada): While a federal law, the Income Tax Act significantly affects estate planning in Ontario by governing the taxation of estates and trusts. It includes rules on the taxation of the deceased’s final income, the treatment of capital gains, and the tax implications of transferring assets to beneficiaries or trusts.

Given the complexity of these laws and their impact on estate planning, individuals in Ontario are advised to consult with legal professionals who practice estate law as well as your accountant. These professionals can provide guidance on creating an estate plan that meets legal requirements and aligns with personal wishes.

Considerations for Estate Planning

When engaging in estate planning in Ontario, several key considerations must be taken into account to ensure a comprehensive and effective strategy. These considerations are vital for safeguarding assets, minimizing legal complications, and honouring your wishes. Here’s an overview of some of the critical aspects to consider:

Legal Requirements for Wills and Powers of Attorney

Understanding and complying with Ontario’s specific legal requirements for drafting wills and powers of attorney is crucial. This includes knowledge about how these documents should be executed, witnessed, and stored. For example, a will must be signed in the presence of two witnesses who are not beneficiaries or the spouse of a beneficiary.

Probate Planning

Consider strategies to minimize probate fees (formerly known as Estate Administration Tax in Ontario), which are calculated based on the value of the estate. This might involve designating beneficiaries on financial products like life insurance policies and retirement accounts or considering joint ownership with the right of survivorship for certain assets.

Tax Implications

Estate planning should also consider potential tax implications, including capital gains tax and the taxation of the estate itself. Strategic planning can help minimize these taxes, preserving more of the estate for the beneficiaries.

Family Dynamics and Needs

Tailoring your estate plan to accommodate the unique needs of your beneficiaries, including minor children, dependents with disabilities, or family members with financial management challenges, is essential. This might involve setting up trusts or specific directives within your will.

Guardianship for Minor Children

If you have minor children, it’s important to consider who will take care of them if both parents pass away. You can specify a guardian in your will, ensuring that your children are cared for according to your wishes.

Healthcare Wishes

A Power of Attorney for Personal Care allows you to appoint someone to make healthcare decisions on your behalf if you become unable to do so. It’s also prudent to consider advance directives or living wills to specify your wishes regarding medical treatment and end-of-life care.

Digital Assets

In today’s digital age, it’s essential to consider how your digital assets, such as social media accounts, online banking, and digital currencies, will be managed. This includes ensuring access to these assets and deciding how they should be handled.

Regular Review and Updates

Life events such as marriage, divorce, the birth of a child, or the acquisition of significant assets can affect your estate plan. Regularly reviewing and updating your estate documents ensures they reflect your current wishes and circumstances.

Key Considerations While Choosing an Executor For Your Will

One of the most important decisions you’ll make while creating your Will is who to appoint as your executor. Your executor will be responsible for carrying out your wishes in your Will and ensuring that your estate is distributed per your wishes. Therefore, choosing someone responsible, trustworthy, and capable of handling an executor’s responsibilities is essential. You might want to consider the following points while making this choice:

Understand the Role of an Executor

First, you should understand this role before considering potential executors. An executor is responsible for managing the estate’s assets, paying any outstanding debts or taxes, and distributing the estate’s assets to the beneficiaries. To perform these duties, they must communicate with family members and beneficiaries, gather all necessary documents, and ensure the estate’s assets are protected.

Consider Personal Characteristics

Choosing an executor is a very personal decision. You need to think about your dynamics with family and friends, whom you trust, who have the necessary skills, and who can handle the role’s responsibilities. Before appointing a family member or friend, you might want to consider their personal characteristics such as honesty, responsibility, and trustworthiness. Can they communicate well and manage your affairs while ensuring they follow your instructions in the will?

Evaluate Financial Acumen

You might want to consider an executor who has good financial acumen. The executor will manage the estate’s assets and ensure that debts and taxes are paid. They might also need to make investment decisions and manage financial accounts. It’s important to choose someone with a good understanding of financial matters or who can consult with professionals to make informed decisions.

Assess Time and Availability

You might have peace of mind by choosing someone available to carry out the necessary tasks since being an executor is a time-consuming responsibility. They will need to communicate with beneficiaries, handle legal documents, and attend meetings therefore, the person you choose as an executor will need to be available to carry out these tasks. If the person you’re considering has a busy schedule or lives far away, it might not be practical to appoint them as your executor, but this depends on your personal situation.

Have a Contingency or Back Up Plan

It’s always a good idea to have a backup plan if your first choice predeceases you or is unable or unwilling to act as your executor. You can appoint a second or third choice as your alternate attorney in your Will or choose a professional executor, such as a trust company or lawyer.

Minimizing Probate Involvement

Strategies to minimize probate are an aspect of estate planning for those looking to streamline the administration of their assets, reduce legal fees, and maintain privacy. In Ontario, as in many jurisdictions, probate is the legal process by which the courts validate a will and involves filing fees based on the value of the assets being probated. Here are some strategies that individuals may consider to minimize the impact of probate on their estates:

Joint Ownership with Right of Survivorship

Joint Ownership with Right of Survivorship is a way of co-owning property where two or more people hold the property together. When one owner dies, the property automatically goes to the surviving owner(s) without the need for probate. It’s a simple way to transfer assets after death and is typically used for assets like real estate, bank accounts, and investment accounts. In Ontario, it’s beneficial for spouses as it simplifies the transfer of assets and gives immediate access to property and funds that might otherwise be tied up during probate. However, it’s essential to understand the legal implications, including potential tax consequences and the loss of autonomy over the asset. Consent from all joint owners is required for decisions regarding the property.

Designation of Beneficiaries

Certain assets, such as life insurance policies, registered retirement savings plans (RRSPs), registered retirement income funds (RRIFs), and tax-free savings accounts (TFSAs), may allow for the designation of beneficiaries. Upon the owner’s death, these assets may be transferred directly to the named beneficiaries outside of the will, thus bypassing probate.

Gifting During Lifetime

An individual may choose to gift assets while they are still alive. This reduces the size of the estate that will be subject to probate. However, it’s important to consider potential tax implications and the loss of control over the gifted asset.

Establishing a Trust

Transferring assets into a trust may also avoid probate. A trust can be created during an individual’s lifetime (a living trust) and can be revocable or irrevocable. Assets within the trust are governed by the terms set out in the trust agreement and can be distributed to beneficiaries without being probated.

Ownership Through a Corporation

For some business owners, holding assets through a corporation can be a way to avoid probate. Upon death, shares of the corporation may be transferred according to the shareholder agreement rather than the will, thus avoiding probate.

Multiple Wills

In Ontario, it’s possible to have more than one will: a primary one for assets requiring probate and a secondary one for assets that do not. This can limit the value of the assets going through probate, potentially reducing the probate fees.

Use of Insurance Products

Certain insurance products can offer probate avoidance as a feature. For instance, some annuities and segregated funds have beneficiary designations, allowing them to pass outside the estate and, therefore, outside of probate.

Summary

When considering these strategies, seeking professional legal and financial advice is crucial, as complex tax and legal implications are often involved. Additionally, these strategies must be tailored to individual circumstances and goals and carefully coordinated to ensure they align with the overall estate plan. It’s also important to regularly review and update estate plans to reflect personal circumstances, relationships, asset composition, and law changes. Probate-minimizing strategies should be approached with a comprehensive understanding of the benefits and potential drawbacks, ensuring the most effective transfer of assets according to the individual’s wishes. By addressing key components such as wills, powers of attorney, and trusts and considering the unique aspects of your family and financial situation, you can develop a comprehensive estate plan that ensures your wishes are honoured, your assets are protected, and your loved ones are provided for. Consulting with legal and financial professionals specializing in estate planning is advisable to navigate the complexities of Ontario’s laws and tax implications, ensuring a secure legacy for your family.

If you need assistance with your wills & estates, contact us today and see how we can help you plan for your future wishes and personal goals.

The information provided above is of a general nature and should not be considered legal advice. Every transaction or circumstance is unique, and obtaining specific legal advice is necessary to address your particular requirements. Therefore, if you have any legal questions, it is recommended that you consult with a lawyer.