Estate planning in Ontario is the process of arranging how you manage your property during your life and how you pass it on after you die. A complete plan uses a few core legal documents. These are a will, a continuing power of attorney for property, a power of attorney for personal care, beneficiary designations, and sometimes a trust. Together these documents control who receives your assets, who makes decisions if you lose capacity, and how much tax and cost your estate carries.

Ontario law sets clear rules for each document. The Succession Law Reform Act governs wills and what happens when you die without one. The Substitute Decisions Act governs powers of attorney. The Estates Act and the Trustee Act govern how an estate trustee administers your estate and how trusts work. Get the documents wrong and a court applies its own default rules instead of your wishes.

This guide explains what each document does, the steps to build a plan, the legal requirements for a valid will, what happens if you die without one, how Estate Administration Tax works, and how to lower it. You will also find a clear answer to common questions families ask.

Need Help with Your Estate Planning?

Speak with an experienced estate planning lawyer in Ontario to get assistance with your matter.

Serving Clients Across Ontario

Remote Services Available

Client Focused & Flexible

What Is Estate Planning?

Estate planning is the act of putting legal documents in place that direct how your property is managed and distributed during incapacity and after death. It is not a single document. It is a small set of documents that work together so that the right people hold authority at the right time.

Many people think estate planning is only for the wealthy or the elderly. That is a myth. If you own a home, hold savings, have minor children, run a business, or simply want to choose who decides your medical care, you benefit from a plan. The point is control. You decide instead of a court or a default formula.

The data shows most people put this off. A 2024 Narrative Research survey found only 43 percent of Canadians have a will, while 53 percent have none. A separate Angus Reid Institute survey found about half of Canadians have no will at all, and a further share hold one that is out of date. Yet most people agree the documents matter. An RBC and Ipsos poll found 91 percent of Canadians think a will is an important part of a plan.

“Most of the estate disputes I see did not start with a complicated family. They started with no plan, or a plan no one updated for a decade. An afternoon of work today saves your family months of stress later.”

— Demet Altunbulakli, Founding Lawyer, Insight Law

Why Estate Planning Matters in Ontario

Estate planning matters because Ontario law fills any gap you leave with its own rules, and those rules rarely match what a person actually wanted. A plan gives you control, lowers cost, reduces tax, and prevents conflict.

- You keep control. You name who inherits, who raises your minor children, and who manages your money and health decisions if you cannot.

- You cut cost and delay. A clear plan reduces legal fees, speeds up administration, and avoids court applications to appoint a decision maker.

- You lower tax and Estate Administration Tax. Smart use of beneficiary designations, joint ownership, and trusts can move assets outside the probated estate.

- You prevent family conflict. Clear instructions remove the guesswork that drives siblings and partners into disputes.

- You protect vulnerable people. A trust can provide for a child with a disability or a beneficiary who is not ready to manage a large sum.

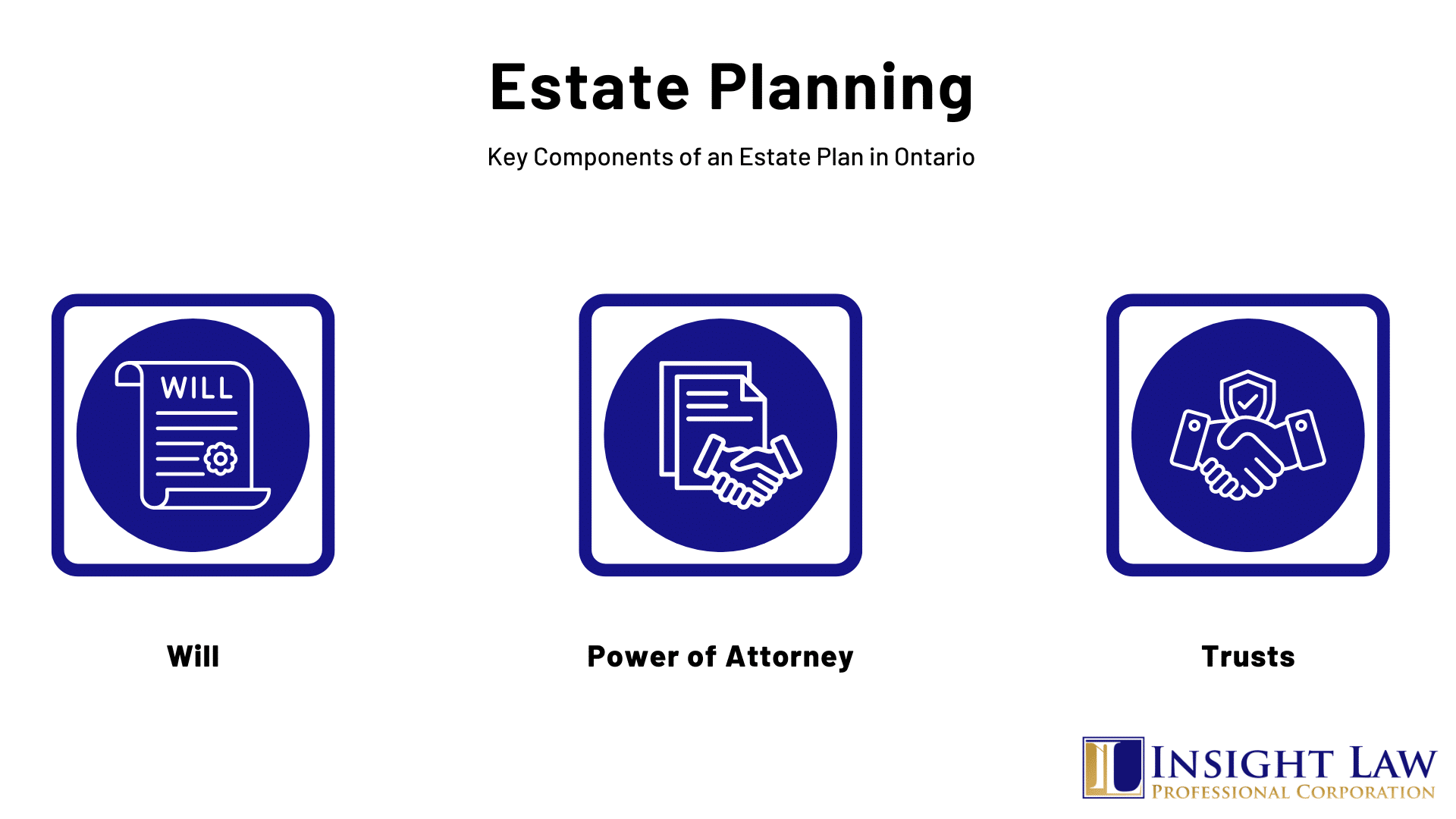

What Documents Make Up an Estate Plan?

An Ontario estate plan is built from a will, two powers of attorney, beneficiary designations, and in some cases a trust. Each document covers a different risk, so most adults need more than one.

Will

A will is the document that directs how your property is distributed after death. It names your beneficiaries, appoints an estate trustee (the modern term for an executor), and lets you name a guardian for minor children. Without a will, Ontario’s intestacy rules decide for you, and you lose the right to name a guardian or a trustee.

Continuing Power of Attorney for Property

This document lets you appoint someone to manage your finances. A continuing power of attorney keeps working even after you lose mental capacity, which is the whole point. Unless the document says otherwise, it takes effect as soon as you sign it. Your attorney can do almost anything with your property that you could do, except make or change your will.

Power of Attorney for Personal Care

This document lets you appoint someone to make health and personal care decisions, such as treatment, housing, and daily care, if you become incapable of making them yourself. You can also record your wishes about treatment so your attorney knows what you want.

Beneficiary Designations

Registered accounts and insurance let you name a beneficiary directly. This includes life insurance, RRSPs, RRIFs, and Tax Free Savings Accounts. When you name a beneficiary, the asset usually passes straight to that person and skips your estate, which means it skips Estate Administration Tax. Keep these designations current, because they override your will for those specific assets.

Trusts

A trust is an arrangement where one person, the trustee, holds and manages property for someone else, the beneficiary. People use trusts in estate planning to provide for a child over time, support a family member with a disability, reduce tax, or keep certain assets out of probate. A trust can run during your life or start through your will after death.

What Are the Steps to Create an Estate Plan?

You build an estate plan by taking stock of your assets and family, setting your goals, choosing the people who will act for you, drafting the documents correctly, and reviewing the plan over time. The steps below give you a clear path.

- List your assets and debts. Write down your home, accounts, investments, insurance, business interests, and debts. This shows the size and shape of your estate.

- Decide who inherits. Choose your beneficiaries and what each should receive. Think about minor children, blended family members, and any dependant who relies on you.

- Choose your people. Pick an estate trustee, an attorney for property, an attorney for personal care, and a guardian for minor children. Name a backup for each role.

- Plan for tax and cost. Identify which assets can pass by beneficiary designation or joint ownership, and whether a trust helps. This is where you reduce tax and Estate Administration Tax.

- Draft the documents correctly. Have a lawyer prepare your will and powers of attorney so they meet Ontario’s signing and witnessing rules and say what you mean.

- Store and share them. Keep the originals safe and tell your estate trustee where to find them. A will no one can locate causes the same problem as no will.

- Review regularly. Update the plan after a marriage, separation, birth, death, major purchase, or business change.

What Makes a Will Valid in Ontario?

A will is valid in Ontario when the person making it is at least 18, has mental capacity, and signs the will following the formal rules in the Succession Law Reform Act. There are two recognized types of will, and the witnessing rules differ between them.

A formal will must be signed at the end by the person making it, in the presence of two witnesses who are both present at the same time. The two witnesses then sign in the presence of the person making the will. A witness, or the spouse of a witness, should not be a beneficiary, because a gift to a witness can fail. A holograph will is one written entirely in the person’s own handwriting and signed by them. It needs no witnesses.

| Feature | Formal (witnessed) will | Holograph will |

| Who writes it | Typed or written, prepared with help | Entirely in your own handwriting |

| Witnesses needed | Two, present together | None |

| Signature | Wet ink, signed at the end | Wet ink, signed by you |

| Best for | Almost everyone | Emergencies only |

Three recent changes matter for anyone reviewing an older plan.

- Virtual signing is permanent. Since January 2022 you can sign and witness a will over live audio and video, as long as at least one witness is a lawyer or licensed paralegal. The signatures still must be in wet ink. Electronic signatures are not accepted for wills.

- Marriage no longer cancels a will. For a marriage on or after January 1, 2022, getting married does not revoke your existing will. The old rule still applies to marriages before that date, so an older will made before a pre 2022 marriage may have been revoked.

- Separation now cancels gifts to a spouse. If you separate, a gift to your spouse and their appointment as your estate trustee are treated as if the spouse died first. Separation here means living apart for three years due to marriage breakdown, a valid separation agreement, or a court order or arbitration award.

A court can also now validate a document that does not meet every formal rule if the court is satisfied it sets out your true intentions. This power applies to deaths on or after January 1, 2022. It is a safety net, not a substitute for signing your will properly.

What Happens If You Die Without a Will?

If you die without a will in Ontario, you die intestate, and the Succession Law Reform Act decides who inherits. The court appoints an administrator, and your assets pass by a fixed formula that ignores your personal wishes, friends, and charities.

A married spouse receives a protected first amount called the preferential share. For deaths on or after March 1, 2021, that amount is 350,000 dollars. After that, the rest is split between the spouse and the children by a set formula.

| Who survives you | How the estate is divided |

| Spouse, no children | The spouse receives the entire estate |

| Spouse and one child | The spouse receives the first 350,000 dollars, then the spouse and child split the rest equally |

| Spouse and two or more children | The spouse receives the first 350,000 dollars and one third of the rest, the children share the other two thirds |

| Children, no spouse | The children share the estate equally |

| No spouse or children | The estate passes to other relatives in a fixed order set by law |

Two points surprise families most. A common law partner does not inherit under these rules, no matter how long you lived together, although they may bring a separate dependant support claim. And a separated spouse is now treated as if they died first, so they do not take a share. These results are exactly why a will matters.

How Do Powers of Attorney Work in Ontario?

A power of attorney is a document that lets you appoint someone to act for you. Ontario has two kinds, one for property and one for personal care, and they follow different rules under the Substitute Decisions Act. Both must be signed in front of two witnesses.

Choose your witnesses with care. Your attorney, your attorney’s spouse or partner, your own spouse or partner, your child, and anyone under 18 cannot witness the document. A disqualified witness can make the power of attorney invalid.

| Feature | POA for Property | POA for Personal Care |

| Covers | Finances, banking, property, bills | Health, treatment, housing, daily care |

| Minimum age to make it | 18 | 16 |

| When it starts | Immediately, unless the document delays it | Only when you become incapable |

| Witnesses | Two eligible witnesses | Two eligible witnesses |

| Can it make your will | No | No |

If you lose capacity without these documents, your family cannot simply step in. They may have to apply to court or to the Office of the Public Guardian and Trustee to gain authority, which costs time and money during a crisis.

What Is Estate Administration Tax and How Do You Reduce It?

Estate Administration Tax, which most people call probate fees, is a tax Ontario charges on the value of the assets that pass through your estate during the probate process. Your estate trustee pays it when applying to the court for a Certificate of Appointment of Estate Trustee. The estate pays the tax, not the beneficiaries directly.

The current rate is simple. The first 50,000 dollars of the estate is exempt. The value above 50,000 dollars is taxed at 15 dollars per 1,000 dollars, which works out to 1.5 percent. Your estate trustee must also file an Estate Information Return with the Ministry of Finance within 180 days of the certificate.

| Estate value through probate | Estate Administration Tax |

| 50,000 dollars | 0 dollars |

| 250,000 dollars | 3,000 dollars |

| 500,000 dollars | 6,750 dollars |

| 1,000,000 dollars | 14,250 dollars |

You can lower this tax by reducing the value that passes through the estate. Each strategy carries trade offs, so get advice before you act.

- Name beneficiaries. Life insurance, RRSPs, RRIFs, and Tax Free Savings Accounts with a named beneficiary usually pass outside the estate.

Hold property jointly. Property held jointly with a right of survivorship passes to the surviving owner. Use this carefully, because a survivorship application and tax can still arise, and joint ownership with an adult child can create disputes.

- Use a trust. Assets placed in certain trusts during your life can pass outside the estate under the trust terms.

- Consider multiple wills. Ontario allows a primary will for assets that need probate and a secondary will for assets that do not, such as private company shares, which can reduce the probated value.

- Gift during your life. A gift made while you are alive is no longer part of your estate, though it can trigger capital gains tax and you give up control.

How Do You Choose an Executor?

Choosing your estate trustee, still widely called an executor, is one of the most important decisions in your will. This person gathers your assets, pays your debts and taxes, and distributes what is left to your beneficiaries. Pick someone organized, honest, and willing to take on the work.

- Trust and judgment. Choose someone honest who will follow your instructions even under family pressure.

- Financial sense. The role involves accounts, taxes, and sometimes investments. Your trustee can hire professionals, but should understand the basics.

- Time and location. Administration takes months. Someone with capacity and reasonable availability handles it better than someone overloaded or far away.

- A backup. Always name an alternate in case your first choice cannot act. You can also appoint a trust company for complex estates.

How Do You Plan for Digital Assets?

Digital assets are the online accounts and files you own, from email and social media to cloud storage, loyalty points, and cryptocurrency. Without a plan, your estate trustee may not be able to find or access them. Treat them like any other asset.

- Make an inventory. List your important accounts and where the records live. Do not write passwords into your will, because a will can become a public document during probate.

- Store access securely. Use a password manager or a sealed record and tell your trustee how to reach it.

- State your wishes. Say which accounts to close, memorialize, or transfer, and who should receive any valuable digital property.

- Plan for cryptocurrency. Crypto can be lost forever without the private keys. Record secure access instructions for your trustee.

Do Business Owners Need Estate Planning?

Yes. Business owners need estate planning more than most, because a business is often the largest and least liquid asset in the estate. A plan keeps the company running and avoids a forced sale. This work overlaps closely with business succession planning, which sets out who takes over and how.

A shareholder agreement can control how shares move on death, a corporate structure can support an estate freeze that caps your tax on future growth, and life insurance can fund a buyout so the family receives value while the business continues. These tools need a lawyer and an accountant working together.

When Should You Update Your Estate Plan?

Review your plan every three to five years, and right away after a major life event. An out of date plan can be as harmful as no plan, because it sends your assets to the wrong people.

- You marry, separate, or divorce.

- You have or adopt a child, or a beneficiary dies.

- You buy a home, sell a business, or your wealth changes a lot.

- Your chosen estate trustee or attorney can no longer act.

- You move to or from Ontario, or tax rules change.

Which Laws Govern Estate Planning in Ontario?

A few main statutes shape every Ontario estate plan. You do not need to read them, but it helps to know what each one controls.

- Succession Law Reform Act. Sets the rules for valid wills, dependant support, and who inherits when there is no will.

- Substitute Decisions Act. Governs powers of attorney for property and personal care, including how they are signed and witnessed.

- Estates Act. Covers how the court appoints an estate trustee and how the estate is administered.

- Trustee Act. Sets out the duties and powers of trustees, including how they invest and manage trust property.

- Income Tax Act (Canada). A federal law that controls the tax on your final return, capital gains on death, and the taxation of trusts.

Frequently Asked Questions

Do I need a lawyer to make a will in Ontario?

No law requires a lawyer, and a handwritten holograph will or a kit can be legally valid. But mistakes in wording, signing, or witnessing are common and often appear only after death, when they cannot be fixed. An experienced lawyer makes sure the will is valid, says what you mean, and works with your tax plan.

How much does estate planning cost in Ontario?

Cost depends on complexity. A basic will with two powers of attorney costs far less than a plan involving a trust, a business, or a blended family. Compare that cost against Estate Administration Tax and the legal fees of fixing an unclear or invalid plan, which usually cost far more.

What is the difference between a will and a power of attorney?

A will takes effect after you die and directs who receives your property. A power of attorney works while you are alive and lets someone act for you if you cannot. You need both, because they cover different risks.

Does my common law partner inherit if I have no will?

Not under Ontario’s intestacy rules. Those rules only recognize a married spouse. A common law partner who is left out may bring a dependant support claim, but that means going to court. If you want your partner to inherit, you must name them in a will.

Can I reduce or avoid probate fees in Ontario?

You can lower Estate Administration Tax by reducing what passes through your estate. Named beneficiaries on insurance and registered accounts, joint ownership, certain trusts, and multiple wills are common tools. Each has tax and legal trade offs, so get advice before you set them up.

How often should I review my estate plan?

Review it every three to five years and after any major life event, such as a marriage, separation, birth, death, or large change in your assets. Ontario law also changes, so a periodic review keeps your plan current.

The information provided above is of a general nature and should not be considered legal advice. Every transaction or circumstance is unique, and obtaining specific legal advice is necessary to address your particular requirements. Therefore, if you have any legal questions, it is recommended that you consult with a lawyer.