Incorporation is a process for businesses in Ontario, indicating the legal establishment of a company under the provincial or federal jurisdiction. This process gives the company a separate legal entity status, distinct from its owners and shareholders. Incorporation in Ontario is regulated by the Business Corporations Act (Ontario), which outlines the legal framework for creating, operating, and dissolving corporations within the province. This article discusses the definition of incorporation, the procedural aspects of incorporating a business in Ontario, and the benefits that this legal structure provides.

What is Incorporation?

Incorporation is the process through which a business becomes a corporation, a separate legal entity from its owners, with its rights, responsibilities, and obligations. The process is guided by legislation, such as the Ontario Business Corporations Act (OBCA), for those who wish to incorporate in Ontario. It involves submitting specific documentation, primarily the Articles of Incorporation, which must detail aspects of the corporation, including its name, directors, share structure, shareholder rights, and operational commencement date. Incorporation is a significant milestone for a business, as it gives it a unique legal identity and allows it to engage in activities such as buying property, entering contracts, and pursuing legal action in its name.

The Articles of Incorporation are the foundation of the corporation’s legal structure, outlining its governance, operational framework, and financial and managerial rights allocation among shareholders. Completing and filing this document, known as Form 1 under the OBCA, is a mandatory step for business owners in Ontario looking to incorporate. This legal process provides the corporation several benefits, including limited liability for its owners, potential tax advantages, and increased opportunities for raising capital. Essentially, incorporation establishes a business as a legally recognized entity with perpetual succession, capable of achieving its objectives while protecting its owners’ assets against the company’s liabilities.

How to Incorporate a Business in Ontario

Incorporating a business in Ontario involves a systematic process governed by the Business Corporations Act (OBCA). This legal framework ensures that businesses are properly registered and structured, offering benefits like limited liability, perpetual existence, and more. Here are typical steps required to incorporate a business in Ontario:

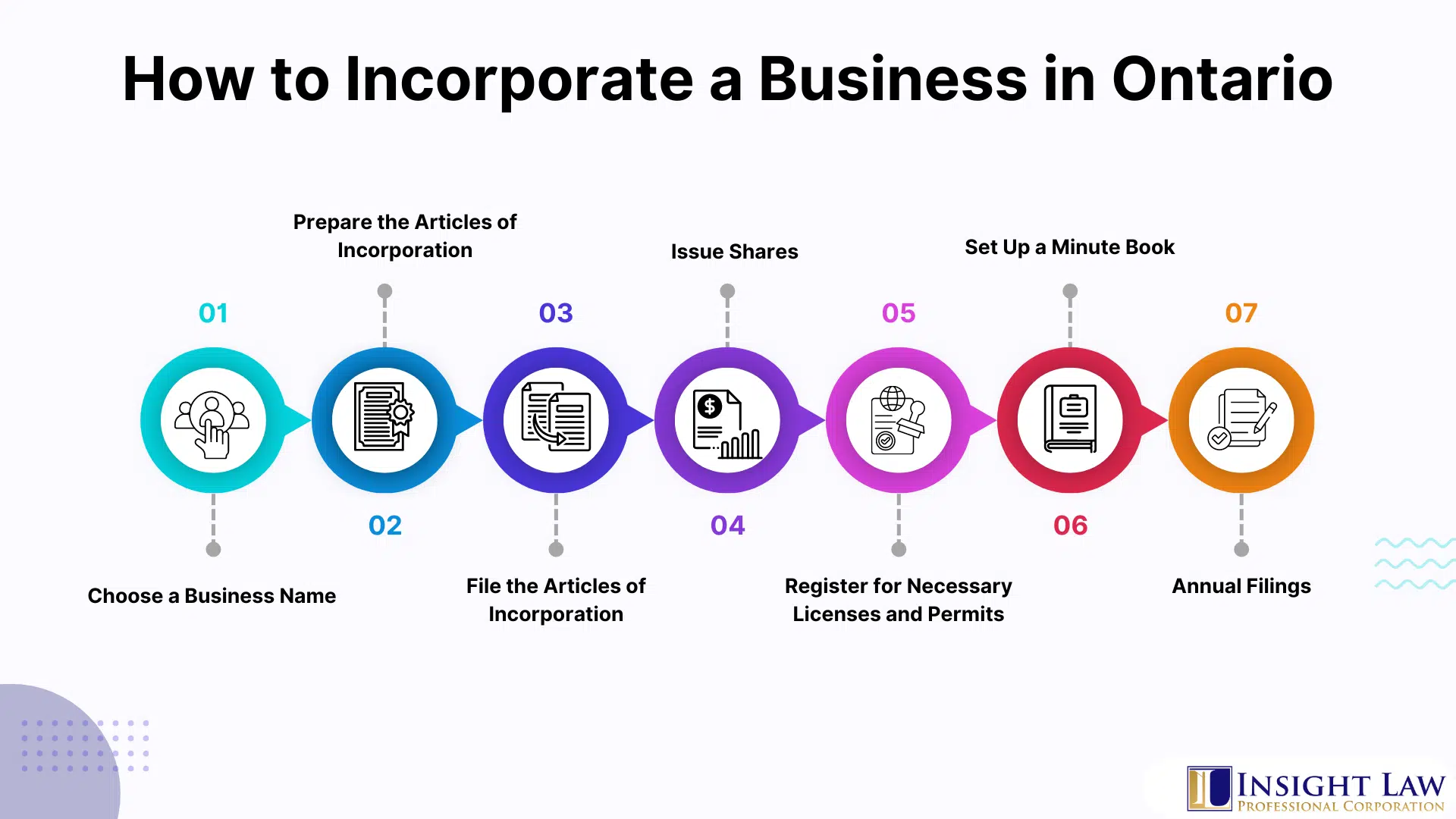

Choose a Business Name

Choosing a business name is the first step of incorporation. This name should reflect the essence of your business, its services, or its products and distinguish you from competitors. Conducting a thorough search, such as a NUANS search in Canada, is imperative to ensure your chosen name does not infringe on existing trademarks or business names. Additionally, consider your business’s future marketing and online presence; the name should be web-friendly, easily searchable, and, ideally, compatible with available domain names for your website. This decision lays the groundwork for building a strong brand and facilitating effective communication with your target audience.

Prepare the Articles of Incorporation

The Articles of Incorporation serve as the corporation’s charter. They must include specific information such as the corporation’s name, its purpose, the types and maximum number of shares that can be issued, restrictions on share transfers, the number of directors, and any limitations on the business activities the corporation may engage in. The Articles must comply with the governing corporate legislation in your jurisdiction, such as the Business Corporations Act in Ontario.

File the Articles of Incorporation

Filing the Articles of Incorporation is a procedural step that officially recognizes the establishment of your corporation under the law. This process involves submitting the completed Articles of Incorporation, along with any required supplementary documents and the appropriate filing fee, to the relevant governmental authority, such as the Ministry of Government and Consumer Services in Ontario. Upon successful submission and approval, the government issues a certificate of incorporation, marking the legal birth of your corporation. This certificate is a critical document, evidencing the corporation’s existence and its authority to conduct business within the framework of the law.

Issue Shares

Issuing shares delineates ownership and raises capital for business operations. When a corporation issues shares, it sells parts of the company to shareholders in exchange for investment. The process involves determining the share structure outlined in the Articles of Incorporation, which specifies the types of shares the corporation is authorized to issue, their value, and any attached rights or restrictions. This action helps accumulate capital and establishes the initial ownership distribution among the founders, investors, and other stakeholders. Proper documentation of share issuance requires recording in the corporate minute book to ensure legal compliance.

Register for Necessary Licenses and Permits

Registering for necessary licenses and permits ensures the corporation operates within legal and regulatory frameworks. This process varies depending on the industry, location, and nature of the business activities. It might include obtaining specific professional licenses, zoning permits, health and safety certifications, or environmental permits. This step is crucial for compliance and to avoid potential legal complications or fines. It’s important to research and understand the specific requirements applicable to your business at both the municipal and provincial levels, as well as any federal regulations that may apply. Timely registration of all necessary licenses and permits legitimizes your business operations. It protects all stakeholders’ interests, including owners, employees, and customers.

Set Up a Minute Book

Setting up a minute book is required to maintain a corporation’s legal and organizational integrity. This physical or digital repository holds documents such as the Articles of Incorporation, resolutions of the directors and shareholders, share certificates, and records of stock transfers. It serves as the official record of the corporation’s governance and operational decisions, ensuring compliance with regulatory requirements and providing a clear history of the company’s legal and financial decisions. Keeping a minute book up-to-date and accurate is a legal requirement in many jurisdictions and a best practice for corporate governance, facilitating transparency and accountability among directors, shareholders, and regulatory bodies. This record-keeping aids in the smooth management of corporate affairs and is invaluable during audits, legal reviews, and potential business transactions such as mergers or acquisitions.

Annual Filings

Annual filings are mandatory to ensure a corporation’s compliance with legal and regulatory obligations and to maintain its good standing with various governmental authorities. These filings usually consist of annual reports, financial statements, and tax returns, and their requirements may differ based on the business’s jurisdiction, industry, and size. Apart from offering a snapshot of the corporation’s financial health, these documents also update the corporate records with current information about directors, shareholders, and company operations. Submitting these filings to the appropriate federal, provincial, or local agencies on time is essential to avoid penalties and sustain the corporation’s legal status.

Additional Considerations

- Legal and Financial Advice: It’s highly recommended to seek legal and financial advice when incorporating a business to navigate the complexities of corporate formation and compliance.

- Federal vs. Provincial Incorporation: Consider whether provincial (Ontario) or federal incorporation suits your business needs. Federal incorporation offers the ability to operate under the corporate name across Canada but comes with different regulatory requirements.

Pros and Cons of Incorporating

Advantages of Incorporation

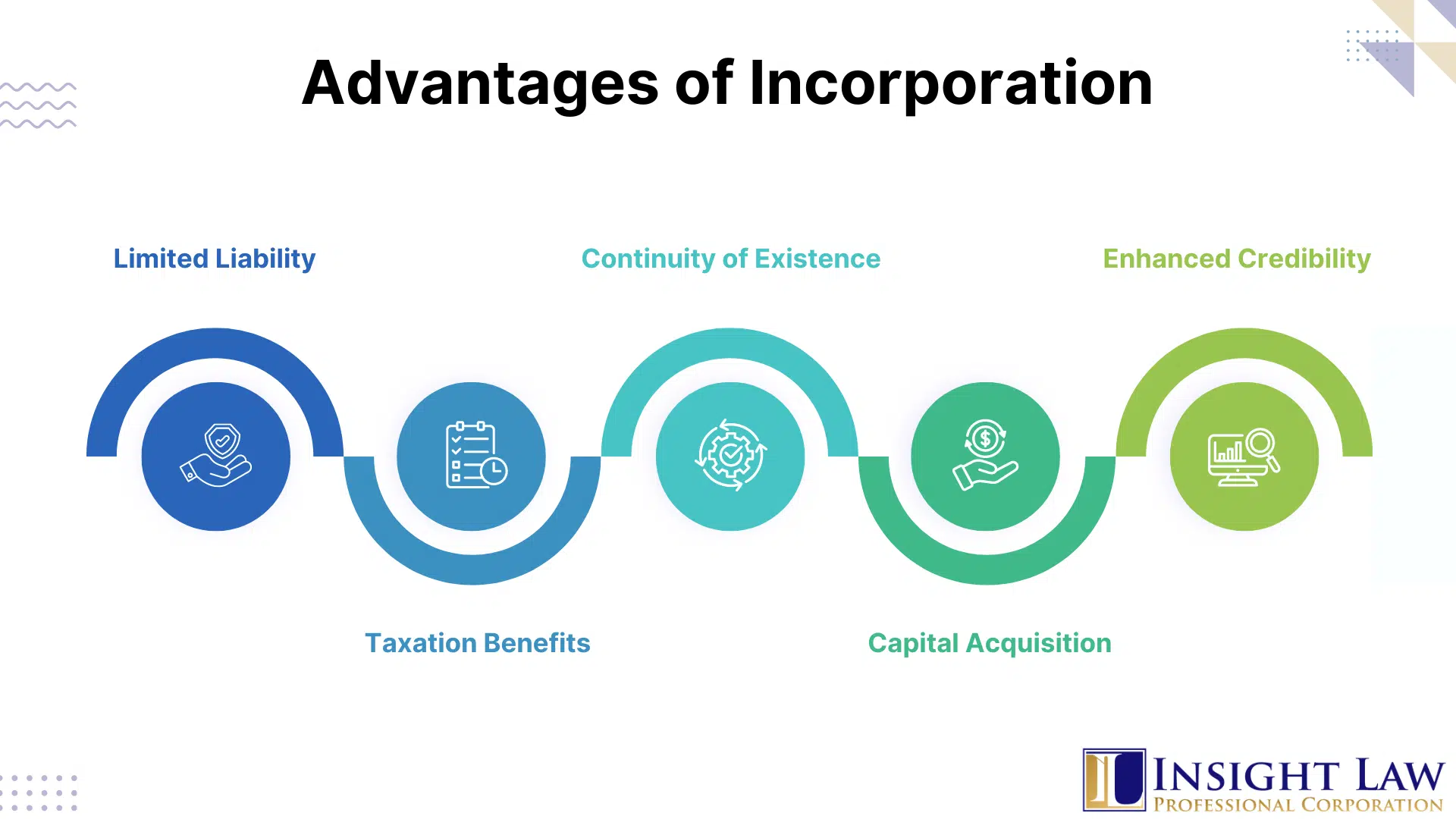

Limited Liability

Incorporation offers business owners a significant benefit of limited liability. When a company is incorporated under the Ontario Business Corporations Act (OBCA), it becomes a separate legal entity from its shareholders and directors. This separation ensures that the personal assets of the shareholders and directors are not at risk due to the debts, obligations, or legal actions taken against the corporation. Shareholders are only liable to the extent of their investment in the corporation, and their personal wealth is protected from corporate liabilities. This is particularly important in cases of bankruptcy or lawsuits. This legal structure provides a significant incentive for entrepreneurship, as it reduces the financial risk involved in conducting business and encourages investment. However, this does not mean a shareholder directly running a corporation cannot be held liable for anything. In some circumstances, those individual shareholders can be held personally liable.

Taxation Benefits

Incorporating a business in Ontario has a lot of advantages in terms of taxation. Incorporated businesses have access to lower corporate tax rates compared to personal income tax rates. They are also eligible for tax incentives and credits unincorporated entities cannot avail themselves of. Small businesses can take advantage of the small business deduction, which can significantly reduce the amount of taxable income. Furthermore, incorporated businesses can defer taxes by retaining earnings within the company instead of distributing them immediately as personal income. Additionally, corporations can optimize their tax situation through income splitting and other strategic financial planning opportunities. These fiscal benefits can considerably lower the overall tax burden and enhance cash flow and reinvestment potential. Consequently, this fosters growth and financial efficiency within the corporate structure. The taxation benefit will vary from individual to individual; therefore, speaking with your accountant to assess your situation is important.

Continuity of Existence

The Ontario Business Corporations Act benefits corporations from continuity of existence. This means that once a corporation is incorporated, it can continue to exist beyond changes in ownership, the death of shareholders, or shifts in management without affecting its legal status or operational continuity. This permanent status is particularly advantageous for long-term business planning and attracting investors, as it assures them that their investment will not be affected by the lifespan of any individual member of the company. As a result, the business can operate indefinitely, creating a sustainable platform for growth, legacy, and transferability of ownership.

Capital Acquisition

As a corporation, it can access various avenues for raising funds that are not typically available to sole proprietorships or partnerships. Being an independent entity, corporations can issue shares and sell equity to investors, which is a crucial mechanism for obtaining investment capital. Additionally, corporations can issue bonds and other debt instruments, providing further options to secure financing. This enhanced ability to raise capital facilitates expansion and growth and provides diversified financial strategies that can be tailored to suit the corporation’s development stages and long-term objectives. Many businesses choose to pursue incorporation to gain such financial flexibility.

Enhanced Credibility

A corporate status can give the impression of a more reliable and professional business, which can be advantageous in dealings with customers, lenders, and suppliers. The formal recognition through incorporation can also help build trust and confidence from stakeholders, leading to better business terms and easier access to credit. Additionally, the corporate structure’s adherence to regulatory requirements further solidifies its reputation as a serious and long-lasting commercial entity.

Disadvantages of Incorporation

Regulatory Requirements

Businesses are required to adhere to strict rules set forth by the Ontario Business Corporations Act. This includes regular filings, statutory meetings, record-keeping, minute book and adherence to corporate governance protocols. These mandatory obligations demand time and resources, making them particularly burdensome for small businesses. Failure to comply with these requirements can lead to penalties, legal issues, and even the dissolution of the corporation. Therefore, businesses need to consider the administrative overhead before deciding to incorporate.

Incorporation and Maintenance Costs

The initial cost of incorporating a business in Ontario includes government filing fees and, potentially, the cost of legal and financial advice to establish the corporation’s structure. Moreover, ongoing costs such as annual reporting, corporate taxes, and professional fees for accountants and lawyers can add to the financial burden.

Double Taxation

This occurs because corporate profits are taxed twice – first at the corporate level and then again at the individual level when they are distributed as dividends to shareholders. This is because a corporation is considered a separate legal entity subject to corporate income tax. When these profits are paid out to shareholders, they are again taxed on their personal income tax returns. Double taxation can significantly reduce incorporation’s financial benefits, ultimately impacting shareholders’ net income. However, it’s important to note that there are various tax strategies and structures, such as the small business deduction, which can help minimize the impact of double taxation. It is important to speak with an accountant to assess the pros and cons of taxation for your situation.

Annual Reporting for Incorporated Firms in Ontario

Annual reporting is a requirement for incorporated firms in Ontario. It encompasses financial and legal requirements to ensure transparency, compliance, and good standing with relevant regulatory bodies. The Corporations Information Act, R.S.O. 1990, c. C.39 handles the legal requirement for annual returns.

Introduction to Annual Reporting in Ontario

In Ontario, incorporated firms are subject to strict annual reporting requirements set forth by the federal and provincial governments. These requirements ensure that corporations operate transparently and are accountable to their stakeholders, including shareholders, creditors, and the government. The annual reporting process involves submitting documents detailing a corporation’s financial status, corporate governance, and compliance with applicable laws.

Key Components of Annual Reporting

- Financial Statements: Corporations must prepare annual financial statements that comprehensively overview their financial performance and position. These statements must be prepared in accordance with Canadian Generally Accepted Accounting Principles (GAAP) and, depending on the size and nature of the corporation, may need to be audited or reviewed by an independent certified professional accountant.

- Corporate Tax Returns: In addition to financial statements, incorporated firms must file an annual corporate tax return with the Canada Revenue Agency (CRA). This return includes information on the corporation’s income and expenses and the calculation of taxes owed or refunds due.

- Ontario Annual Return: Corporations conducting business in Ontario must file an Ontario Annual Return with the Companies Branch of the Ministry of Government and Consumer Services. This return is usually filed through the Corporations Information Act Annual Return (CIA AR) and is due within six months of the corporation’s fiscal year-end.

Deadlines and Filing

The deadlines for annual reporting can differ depending on the specific requirement. Financial statements and corporate tax returns should be filed within six months of the corporation’s fiscal year-end. The Ontario Annual Return also follows this timeline. Corporations must be aware of these deadlines and plan accordingly to avoid penalties.

Penalties for Non-Compliance

Failure to meet annual reporting requirements can result in significant penalties for incorporated firms. These may include fines, the revocation of corporate status, and other legal repercussions. Furthermore, compliance may positively impact a corporation’s ability to conduct business, obtain financing, or enter into contracts.

Annual reporting is a part of corporate governance that every incorporated firm in Ontario must follow. It helps ensure transparency, accountability, and compliance with legal obligations related to financial reporting. Corporations must diligently prepare accurate reports and meet deadlines to avoid penalties and maintain their standing. Hence, corporations should seek professional advice to navigate the complexities of annual reporting requirements effectively.

Incorporated firms in Ontario should consult with legal and accounting professionals to ensure their annual reporting processes are handled efficiently and comply with all relevant regulations. This proactive approach will help safeguard the corporation’s integrity, facilitate sustainable growth, and uphold its responsibilities to stakeholders.

Benefits of a Holding Corporation

Holding corporations has become increasingly popular in today’s corporate world due to their strategic advantages. A holding corporation is designed to own assets, stocks, or other investments instead of engaging in business operations. This approach aligns with various legal frameworks and provides benefits to businesses. Three primary benefits include:

Asset Protection

One of the most significant benefits of a holding corporation is safeguarding assets. By holding valuable assets such as intellectual property, investment shares, or real estate, the holding corporation effectively separates these assets from the operational risks of running a business. This structure is crucial in protecting assets from potential liabilities or claims arising from business operations. The legal separation, structured under corporate statutes like the Ontario Business Corporations Act, R.S.O. 1990, c. B.1, ensures that assets held in the holding corporation are separated from subsidiary liabilities.

Tax Efficiency and Deferral

Tax management is another area where holding corporations offers substantial benefits. Under the Income Tax Act of Canada, holding corporations can capitalize on lower corporate tax rates compared to personal tax rates. Moreover, they provide opportunities for tax deferral. Earnings and profits generated by subsidiary companies can be channelled as dividends to the holding corporation, which are taxed at the corporate rate. This mechanism allows for the deferral of additional taxes until earnings are distributed to individual shareholders, thus providing an efficient way to manage and reinvest profits.

Simplified Estate and Succession Planning:

Holding corporations simplifies transferring business interests, particularly in estate and succession planning. Transferring ownership through a holding corporation can be more streamlined, as it often involves the transfer of shares of the holding entity rather than individual assets. This process can reduce costs and complexities associated with asset transfers. For estate planning, a holding corporation provides a structured approach to transferring wealth and business interests, aligning with estate laws and offering a clear path for future generations.

Summary

Incorporation in Ontario provides a framework for businesses to operate within a legal structure that offers advantages, including limited liability, potential tax benefits, and enhanced credibility. The process involves considering the business name, structuring the corporation through the Articles of Incorporation, and complying with ongoing regulatory requirements.

Insight Law Professional Corporation is a corporate law firm. If you are searching for guidance from a Toronto Incorporation Lawyer, contact us and see how our firm can help you.

The information provided above is of a general nature and should not be considered legal advice. Every transaction or circumstance is unique, and obtaining specific legal advice is necessary to address your particular requirements. Therefore, if you have any legal questions, it is recommended that you consult with a lawyer.